Fairfax Financial Holdings: Large Upside Potential with Minimal Downside

Member write-up by: Alex Middleton

Introduction

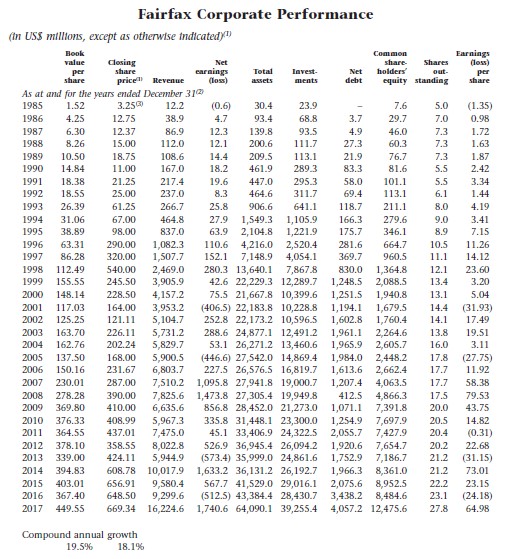

In the past 10 years Fairfax Financial has achieved what can easily be considered sub part returns, however I believe that the company will outperform the S&P significantly in the next 10 years as a result of the improved rate of return on their investment portfolio and a multiple expansion on their stock. One of the main reasons that their stock is undervalued today is because people are anticipating that Fairfax’s growth will underperform in the future as it has in the recent past. Fairfax’s entire history however tells a different story. From 1985 to 2017 Fairfax achieved a compound annual growth rate of 19.5% on their book value (Source: 2018 Annual Report). This is a tremendous achievement over the span of 3+ decades which many people seem to forget. Fairfax has (until recently) been heavily hedged against equities, at a time the S&P continued to grow to unprecedented levels year after year and this underperformance is still very fresh in people’s memories.

The hedging has always been justified by Fairfax management by reiterating their goal of protecting shareholders capital against (what they perceived) as a major risk of deflation in the global economy, which was not entirely unreasonable given how much money the Federal Reserve injected into the economy post 2008. Over the course of the past 10 years Fairfax has been quietly building their set of tools to take advantage of the next big opportunity that the market offers them. From 2008 to 2017 they have managed to compound their investments per share by 2.4% and compound their book value by 5.4% per year. At today’s price you are paying approximately 1.1x book for the business. In this article I will summarize why I believe Fairfax is a very good investment opportunity for investors today.

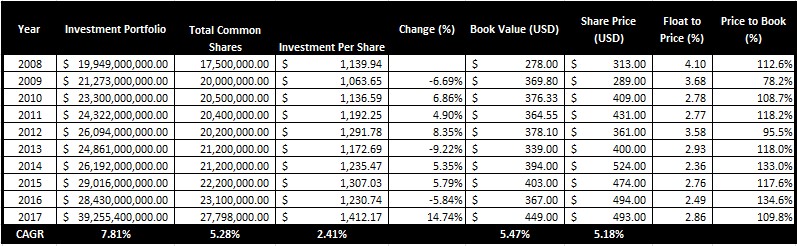

Investment Portfolio

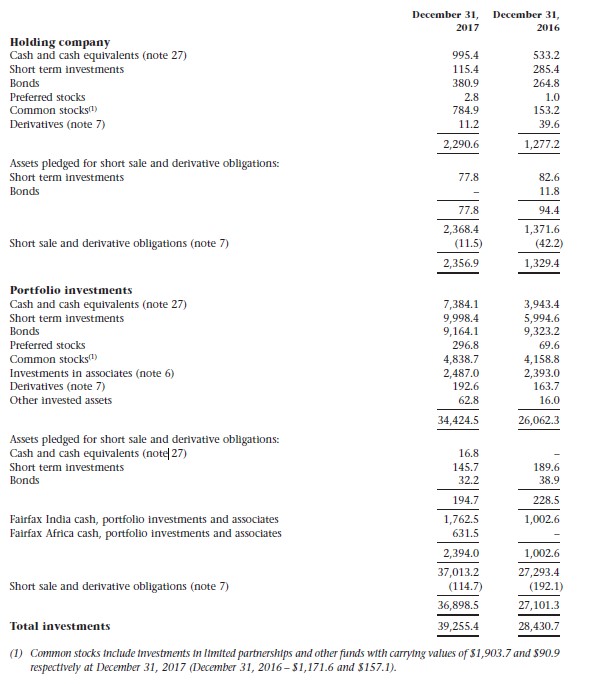

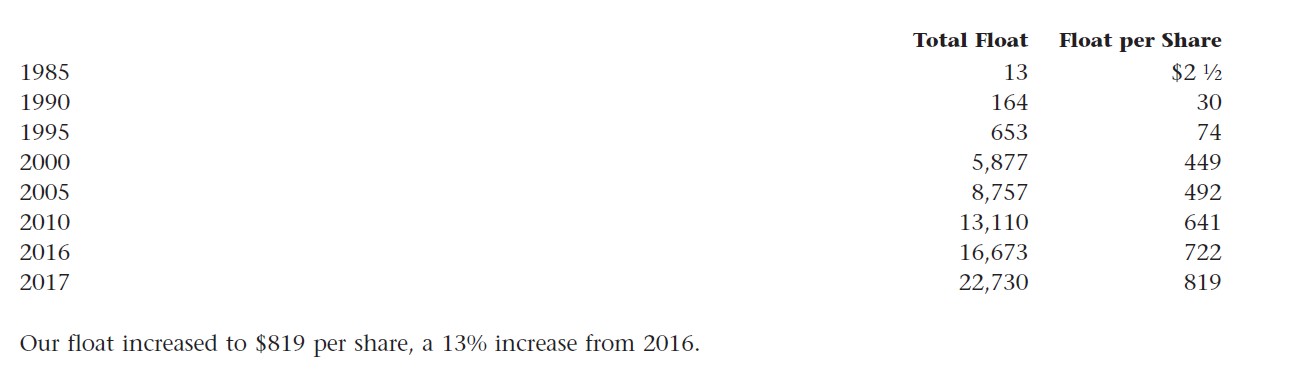

Fairfax’s current investment portfolio is comprised of a combination of book value, debt and insurance liabilities (float) and is worth $39.2 billion as of Q4 2017 (Source: 2018 Annual Report). This amount currently works out to $1412 per common share ($1250 per common share less debt and goodwill) where about $819 per common share is made up of their insurance float (Source: 2018 Annual Report). When a value investor finds opportunities to put this amount of money to work at a decent return, the relative impact on shareholders’ equity can be dramatic. Recently Fairfax has removed a considerable amount of their equity hedges from their portfolio and is now sitting with about 50% of their investments in cash. As with many other value investors who are expecting the next big opportunity in stocks to come in the near future, this sort of “war chest” is exactly what they need in order to surpass their previous 10 years investment performance.

In this year’s shareholders letter Prem Watsa had indicated that buying back shares would be done more aggressively in the future than in the past. At today’s stock price of $495 or 1.1x book value and with $17.3 billion in cash and short term investments, this may be the best allocation of their money in today’s overpriced equity markets. This could allow for their total share count to be drastically reduced by using only a fraction of their entire investment portfolio and allow long term Fairfax investors to realize the benefits of improved investment returns in the future, without compromising their ability to take advantage of a collapse in the equity or bond markets. If Fairfax truly hopes to reach a 15% return on their book value, then they must also believe that their shares are considerably undervalued at the moment, and buying shares is a very tax efficient way to return money to shareholders.

Insurance Businesses

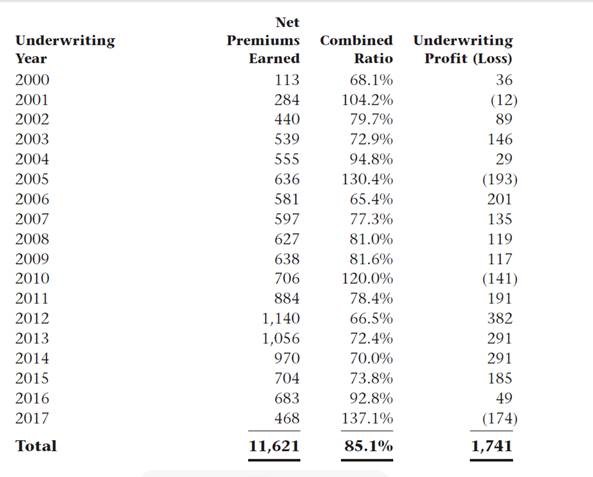

While in many ways you could compare Fairfax to Berkshire Hathaway (NYSE : BRK.A) , they are still two very different companies in many aspects. Berkshire has a large portfolio of insurance companies that are very important to the overall performance of the company, but overtime their non-insurance companies have slowly become a bigger portion of their business. Fairfax on the other hand is still very much an insurance holding company and like many of their industry peers, they incurred significant catastrophe losses from Hurricanes Irma, Hurricane Maria, Hurricane Harvey etc. in 2017 which resulted in an overall combined ratio of 137%. Outside of these losses however they have averaged a combined ratio of 85.1% since 2000. This performance is considered outstanding in the insurance industry because not only have they managed to turn a profit on their insurance operations, they have also had the luxury of using the float (insurance liabilities) as a tool for investment purposes. Based on history, these unprofitable years will again occur in the future, but there is no reason to believe Fairfax cannot continue to achieve an average combined ratio of 95-100% over the next 10 years.

Book Value

On December 31, 2017, common shareholders’ equity was $12.4 billion, or $449.55 per share, compared to $8.4 billion, or $367.40 per common share, on December 31, 2016. Most of this gain in book value can be attributed to the reduction in their ownership in insurer ICICI Lombard from 35% to 9.9% (Realized After Tax Gain of $930 Million) and sale of First Capital to Mitsui Sumutomo (Realized After Tax Gain of $1 Billion). At today’s price of $495 USD you are paying a multiple to book value for Fairfax of 1.1x which may be quite a bit less than if you did a sum of parts of Fairfax’s individual insurance companies. In general many insurance companies are valued as low as their book value however Fairfax paid up to 1.3x book value for Allied World in 2017 which might indicate that the market value of their big insurance companies are worth significantly more than what is being recorded on the balance sheet. Most of the parts of Fairfax are fairly liquid if you think of a situation in which they were forced to sell off the pieces individually, so I am comfortable that they should are not worth anything less than 1x book at the minimum, and an appropriate value for Fairfax based on book could be as high as 1.3x depending on what you think they will be able to do with their investment portfolio in the next 10 years.

Valuation

I’ll admit a good portion of this investment thesis is based on the long term investment and operational record of Fairfax’s management and that they will once again start outperforming. Fairfax has mentioned many times that they hope to compound shareholder book value by 15% going forward under the assumption that they can achieve a 7% return on their investment portfolio and hold a 95% combined ratio in their insurance companies. Given the size of their investment portfolio, historical investment performance and stable insurance companies, I can’t foresee how their performance would be any worse than the previous 10 years. In the situation where Fairfax achieves the most reasonable outcome of between 5% and 7% return on their investment portfolio (Equivalent of $51-$71 after tax per share or 11%-15% return on book) their stock price should trade anywhere between about $765 and $1065 assuming a 15x multiple. I would recommend buying the stock at today’s price level of $493 USD in anticipation of Fairfax successfully investing their portfolio over the next 10 years with a potential upside to the stock of up to $1065 and a low probability – minimal downside of 1x common shareholders’ equity per share of $449. One of these days eventually Fairfax will do very well but one shouldn’t expect any immediate gains overnight.

Want to talk Fairfax Financial with fellow members? Click here to see the stock’s discussion thread.