The write-up you’re most likely to be interested in is the Value Investors Club post from earlier this year. However, that site is down as I’m writing this. So, I can’t link to it. You can search for MLP on the site to find it.

As you can see, Maui Land & Pineapple is not in any sense an undiscovered stock. It’s gets written about a lot by value investors.

If you have any questions about the company, information you’d like to share, links to other write-ups on MLP you know about, etc. please do so below.

Maui Land & Pineapple (MLP) owns real estate on the island of Maui (which is in Hawaii). The company has 22,800 acres of land carried on its books at prices dating back to the 1911 to 1932 period. So, book value is meaningless here. The total size of the land holdings is also meaningless here. Of the 22,800 acres, 9,000 acres are conservation land. That leaves only 13,800 acres of potentially productive land. Almost all of that (12,900 acres) is zoned for agriculture.

That leaves 900 acres zoned for residential use.

Let’s compare those 900 acres of land to the company’s enterprise value to get a sense of just how expensive this stock is on a price per acre basis. The company has 19.18 million shares outstanding. As I write this, the stock price is $11.40 a share.

Since we’re talking shares outstanding, I’m going to pause to discuss liquidity. I may run managed accounts focused on the most illiquid stocks out there (because I believe stocks with wide bid/ask prices tend to be less efficiently priced than stocks that trade constantly at almost no spread), but I know some members of Focused Compounding prefer more liquid investments. MLP should be liquid enough for everyone. The stock trades about $300,000 worth of shares per a day. It’s listed on the New York Stock Exchange.

Now, a bonus aside for those interested in ultra-illiquid stocks: if you’re interested in Maui Land & Pineapple after reading this write-up, you should definitely check out is closest “peer” of sorts – Kaanapali Land LLC (KANP). KANP is an illiquid (it trades about $2,000 worth of stock on an average day) over-the-counter stock. I’m not going to discuss KANP here. However, what land it owns – which I think is much more speculative and possibly worth much less than the land I’m about to discuss owned by MLP – is only something like 4 miles from the land we’ll be talking about here.

Now back to the enterprise value calculation. MLP stock is at $11.40 a share and there are 19.18 million shares outstanding. So, that’s $11.40 times 19.18 million equals $219 million. You can find the company’s 10-Q on EDGAR and decide how much net cash or net debt to add to that $219 million to get the correct enterprise value. There’s a tiny bit of cash, a tiny bit of debt, some retirement benefit obligations, etc. For our purposes, all balance sheet items excluding the 900 acres of residential zoned land are a rounding error. So, I’m going to round the market cap up from $219 million to $220 million and call that the enterprise value.

Now, we can calculate the price ratio that matters most here. It’s not price-to-book (meaningless because the land is carried at at 1911 to 1932 values) or price-to-earnings (also meaningless because it includes land sales which are very lumpy from year-to-year). It’s enterprise value per acre. So, that’s $220 million in EV divided by 900 acres of …

To Focused Compounding members:

One of the most difficult things for investors to deal with is to watch other get richer faster than you. In the stock market, the same choices are available to everyone. So, if someone is up 20% this year, they are up 20% purely on a collection of opportunities you passed on. Two things make this even tougher for the people reading this memo. One, you judge yourself on your relative results versus a benchmark like the S&P 500. Two, you judge yourself on a yearly basis. Even if your process is superior to that of most other investors – there’s a decent chance you’re lagging this year. Does that mean you’re a failure as an investor? Is it even realistic to set the bar as high as beating a benchmark each and every year?

Let’s think about this another way. Let’s remove the idea of you from this analysis. Instead let’s imagine we are evaluating not an investor but an investment strategy. And, to make this easier, let’s set the pace horse a lot slower. Investing in the S&P 500 is not a bad strategy long-term. What is a bad strategy? Putting 100% of your savings into a commodities basket month after month. History shows that holding a basket of commodities indefinitely barely keeps up with inflation. So, if you continue to make a 100% commodities wager month after month for the rest of your working life you are almost certain to underperform the person who makes a 100% S&P 500 index wager month after month for the rest of his working life. In fact, based on the very long-term past record the annual real edge your neighbor would have over you if he invested 100% in a stock index fund and you invested 100% in a commodities basket would be greater than the house’s edge on a single game of baccarat, blackjack, roulette, or craps.

To simplify this hypothetical, let’s say you get only one investment choice your whole life. Instead of picking specific investments as the years go by – you only get one choice at the start of this 30-year period. And that choice is a strategic choice. You can either pick the 100% stocks strategy or the 100% commodities strategy. You can’t switch. Will there be years in which you regret taking the 100% stocks strategy? In a sense, yes. A basket of commodities will – in some of the next 30 years – outperform a basket of stocks. Yet, to say you would – in those years – actually regret your initial choice of the 100% stock strategy is like saying a casino would rather be the player than the house. If the casino knew the future of each hand, each night of play, etc. – I guess you could say that. However, what exactly is it that an investor is actually regretting in his poor relative performance years? He’s regretting not switching strategies from a long-term superior strategy to …

To Focused Compounding members:

As a stock picker, when you’re first faced with the decision to buy or not buy a stock – it seems like a complicated question. Consider the mental math problem of 54 times 7. There are a couple ways of tackling this problem. The simplest though is to multiply 50 by 7, getting 350 and then multiply 4 by 7 getting 28. You add 350 to 28 and get 378. There are several ways of solving this problem. However, in actual practice, the method I laid out is the best. Sure, the answer is exactly the same as if you first multiplied 7 by 4 getting 28 to start. However, if your brain hits a snag while keeping track of the problem you’re solving you would, in the first case, already have the number 350 and therefore be just 7.5% below your target even if you gave up right then. Using the second method, your first step would only get you to the number 28. You’d be 92.5% below your target at that point and the only other bit of information you’d have is that the answer “ends in 8”. Knowing an answer ends in 8 might be useful on a math multiple choice test – but not much else. However, being just 7.5% shy of of an answer – and knowing you’re below the answer, not above – is often helpful in real life. The step “50 times 7” is simple and informative. The step “4 times 7” is just as simple, but far less informative. When analyzing something, the step you want to take next is the one that maximizes both the simplicity of the step and the value of the information you get by performing that step.

I said “…the only other bit of information you have…” back there. And that might be a helpful way to think of solving stock analysis problems: as taking steps that get you “bits” of information. What bit of information is most valuable to me? At the end of the day, a stock picker needs to decide only two things about a stock: 1) buy or don’t buy and 2) how much to buy. How much of your portfolio to put into a stock is an incredibly complex problem. A simple rule like always putting the same amount of your portfolio into every stock you buy can set that complex problem aside while you try to solve a simpler problem. Even then, you’re left with the complex problem of trying to guess what compound annual return this stock will provide should you buy it. How can you simply this problem? Well, you can take a problem that requires a quantity as the answer and turn it into one that requires only a greater than or not greater than answer. At any point in time, your portfolio will already have stocks in it. Assume you have no cash. You …

Monro (MNRO) is a large chain of auto shops providing a wide range of automotive service and repair work in the United States with company-operated stores servicing 6.2 million cars in the fiscal 2018 year ending 03/31/2018. While originally based out of the Northeast, Monro has been executing a roll-up strategy for decades, slowly widening their coverage as they expand both south and west. As of the end of fiscal year 2018, Monro had 1,150 company-operated stores, 102 franchised locations, 5 wholesale locations, 2 retread facilities, and 2 dealer-operated stores. These locations are spread across 27 states and operate under the following brands: Monro Muffler Brake & Service, Car-X, Tread Quarters Discount Tire, Mr. Tire, Autotire Car Care Center, Tire Warehouse, Tire Barn Warehouse, Ken Towery’s Tire & Auto Care, and The Tire Choice.

One of the largest operators of automotive repair and service shops in the US, Monro has used a roll-up strategy to become one of the lowest-cost operators by building an increasingly dense network of auto shops that result in improved economics through the sharing of distribution, marketing, and management costs. Further, as a large purchaser of aftermarket auto parts, Monro enjoys relatively more bargaining power than most of its competitors. These factors have resulted in increasingly superior margins, decent economics, and consistently competitive prices for its customers. While this acquisition-based strategy has been in the works for decades, the industry is still incredibly fragmented and offers a long runway of growth for Monro to continue to deploy capital in acquiring and developing new shops. This will serve to further improve operating efficiencies, and thus economics, and allow Monro to continue to offer its work at very competitive prices.

In addition to the long runway of growth, Monro is a durable business with strong and stable cash generation. This is because people must continue to service their vehicles in all economic climates. Historically, Monro has held sales, margins, and cash flow strong during downturns. In fact, Monro is somewhat countercyclical in that when new car purchases are halted, repairs are increased. This allows Monro to do especially well in a downturn. As we approach a decade-old bull market, the new cars sales cycle begins its descent, the average age of vehicles on the road increases, the number of vehicles on the road increases, the shift away from DIY auto work continues, and the number of service bays decreases, there are a confluence of factors that bode well for Monro’s future earnings power.

The Business

Monro’s business is broken into two main categories: undercar service and repair and tire sales and service. Monro categorizes its shops as either service stores or tire stores. In reality, there is a large degree of overlap in these locations where you see the service stores doing tire work and the tire stores doing non-tire service work. For example, in 2018 23% of service stores’ revenues were related to tires, and 40% of tire …

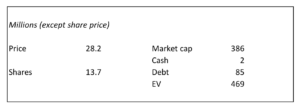

Hamilton Beach Brands Holding Co should not be a completely new stock to Focused Compounding members – but, for those who may be new I will provide a bit of a background. Hamilton Beach Brands Holding is the stock that was spun off from NACCO Industries (NC) last year, which of course NC is the stock that Geoff put 50% of his portfolio in. Hamilton Beach Brands Holding Co opened up post spin at $32.86 and quickly ran to $41.00 per share, only to fall back down to a low of $20.97. With HBB currently sitting at $28.20 about 8 months after the spinoff took place, we felt like it was worth another look.

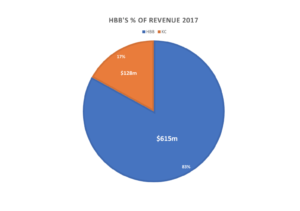

Hamilton Beach Holdings is an operating holding company that has two business segments: Hamilton Beach Brands (HBB) and Kitchen Collection (KC). HBB sells small electric household and specialty houseware appliances to brick and mortar and through e-commerce channels in about 50 different categories. They sell through Walmart, Target, Kohls, and Amazon. If you’ve ever been down a Walmart blender aisle I’m pretty confident you have come across their products. They make blenders, toaster ovens, coffee makers, indoor grills, etc. HBB’s business model is asset light because they outsource all of their manufacturing to 3rd parties in China which allows them to earn a high ROC (total CapEx for 2018 is only expected to be $10.5m, or about 1.7% of revenue). If you think about the staying power of the products that they sell it’s pretty safe to say we will still be using blenders, crockpots, and toasters 10 years into the future.

Kitchen Collection is the problem child in the business that is a specialty retailer of kitchenware in outlet and traditional malls throughout the United States. Management talked about their challenges in their last quarterly conference call, which they’re handling those challenges prudently. Their revenues fell $4.6m in the first quarter (their revenue comes from selling specialty kitchenware items in their retail stores) and management said in the conference call that they expect 70% of their leases to be one year or less by the end of 2018. Although KC is in decline mode with no favorable happy ending in sight, management is being proactive by not investing much capital into the business. Total CapEx for KC is expected to be only $500k for 2018.

For the investment case, I factored in zero value for KC.

Revenue breakdown from HBB’s most recent 10k:

What’s it worth?

Management has long-term objectives (which excludes KC) of $750m – $1B in sales with an EBIT profit margin of 9%, which would translate into an EBITDA margin of 10%. We can use this as a base in our minds, but to start let’s run through a few different scenarios to see what HBB could be worth. In the examples below, I grew revenue first by 2% for the next 5 years in addition to growing EBITDA margins to their target …

To Focused Compounding members:

Since I read “Fortune’s Formula” and “A Man for All Markets” this past week, let’s talk blackjack. In blackjack, the player has an advantage over the casino if he’s counting cards. A card counter can bet nearly the minimum when he suspects the rest of the deck has cards unfavorable to him in higher proportion than a fresh deck and he can bet nearly the maximum when he suspects the rest of the deck has favorable cards in a higher proportion than a fresh deck. Applying this to stocks, let’s say you’re convinced Wells Fargo is a safe bank and Bank of the Ozarks is a risky bank. You have $10,000 to invest in bank stocks. These are the only two bank stocks you know anything about. You have one question: what happens if instead of taking your $10,000 and putting $5,000 into Bank of the Ozarks and $5,000 into Wells Fargo you instead put $1,000 in Bank of the Ozarks and $9,000 in Wells Fargo. You still start off with $10,000 worth of bank shares, but now you are acting like a card counter – betting nearly the maximum when you think the rest of a deck (Wells Fargo’s future) is favorable and betting nearly the minimum when you think the rest of deck (Bank of the Ozarks’ future) is unfavorable. How important is your decision to split your money 10/90 in favor of Wells Fargo?

Let’s say the chance of Wells Fargo stock going to zero in any one year is 0.5% and the chance of Bank of the Ozarks going to zero in any one year is 5%. Over a single year, a bigger annual upside – especially in the form of a quicker catalyst – can make up for a stock being 10 times riskier. Stocks are volatile. And any extra chance of a 50% pop in the stock’s price this year could overcome a 4.5% difference in the rate of catastrophe. So, if you frame your own investment lifetime as lasting only a single year – the math says it’s perfectly fine to bet as much on Bank of the Ozarks as on Wells Fargo. Catastrophic failure is not a big deal over one year. And you’ve promised yourself you’ll only play one hand. You’ll buy both Wells and Bank of the Ozarks today and sell twelve months from today no matter what. Whatever result you get won’t compound. That makes failure cheap. And if there’s some upside catalyst you see for Bank of the Ozarks this year – that catalyst could overcome the 4.5% greater chance of catastrophe this year. But, that’s framing the choice as a one-year bet. Buffett has owned Wells for 27 years. So, let’s ask: what is the difference between a 99.5% annual survival rate and a 95% annual survival rate if you’re committed to letting each bet ride for the full 30 years? Now failure isn’t cheap. It’s expensive, because it kills compounding. If you …