I took a quick look at Hamilton Beach Brands after reading about it in some of Geoff’s articles. In the 10-K, the company segments profits by NACoal, KC, NACCO & Other, and HBB. So, I’m talking about HBB here and I’m just crunching numbers without doing any sort of qualitative analysis.

5Y median Return on Tangible Capital ~23%.

HBB Revenue ~$600MM.

5Y median revenue growth 3.8%, so estimate 3-4% moving forward.

5Y median operating margin ~7%.

Normalized operating profit ~$42MM.

5Y median CFFO / operating profit is 84%, so normalized CFFO = $35MM.

Maintenance Capex ~$5MM.

FCF ~$30MM.

Assume forward market return of ~8%. Conservatively, HBB should grow revenues by about 3% per annum. So, a fair multiple in today’s terms is 20x.

Multiple of 20x on $30MM FCF is $600MM.

I would want a minimum of a 10% annual return, so I wouldn’t pay more than a 14.3x multiple (1 / [10% – 3% annual growth]). Hence, I’d want to pay around $425MM to consider an investment.

You can read a new article over at GuruFocus that I wrote discussing the lignite coal mining business (NACoal) that will be left over once NACCO spins off its Hamilton Beach brand of small appliances.

“The company is involved in operating lignite (again that’s “brown”) coal mines for a few major customers. These customers are usually power plants of some kind. They sit very, very near (in some cases, basically on top of) the coal deposit that NACoal is working. I was able to confirm this to my satisfaction by going online and getting satellite images of NACoal’s five biggest mines. Using those images, I can see where the customer’s plant is in relation to the surface mining activity.

I’ve never researched a coal miner before. However, I have researched two companies related to coal mining…”

“With respect to CAKE and its same-restaurant sales decline, do you have any thoughts on the following:

1. The strength / source of its economic moat?

2. Will the cost spread between eating at home and eating away from home narrow, and if so, what will cause it to do so?

3. Are you worried about declining foot traffic at malls, and brick and mortar stores in general, as it pertains to CAKE?

I’m also wondering if you still feel The Restaurant Group is a potentially attractive idea?”

First, an aside: For those who don’t know, what he’s talking about in #2 is the fact that food prices in U.S. supermarkets have been falling for about 2 years even while food prices in U.S. restaurants have been rising. That’s historically rare. In fact, the recent rate of change in the relative price of food in supermarkets versus food in restaurants may be historically unprecedented. Other things equal, such a relative price change obviously causes restaurant traffic to fall and supermarket traffic to rise.

Back to the questions…

1) I don’t think Cheesecake Factory (CAKE) has a moat. Everyone goes to multiple restaurants. The most successful restaurant chains do a good job of compounding wealth for shareholders and earning high returns on capital. But, no restaurant is insulated from competition with others. So: no moat.

2) Yes. At some point, prices of food in supermarkets will rise faster than prices of food in restaurants. Several publicly traded supermarkets had EPS declines of 10% to 20% this year. That won’t continue indefinitely. At some point, they will have to open fewer new stores, close some existing stores, and raise prices. Food at home prices have fallen because retailers have accepted pricing that earns them less money. What’s happened is not that food costs are down. It’s that supermarket profits are down. The cycle will get worse as long as rivalry in food retail gets more intense and then it will get better only once rivalry in food retail gets less intense. Right now, food retailers are more intense rivals than restaurants. I haven’t seen anything that changes costs in food. I’ve just seen supermarkets and other retailers lowering prices without lowering costs – and thereby lowering profits for themselves and their competitors.

3) Yes. Declining traffic to malls is the biggest risk for Cheesecake Factory. Management thinks it can grow from about 200 locations in the U.S. to about 300 locations. That means finding another 100 good locations for a Cheesecake Factory where there isn’t already a Cheesecake Factory. If there is a societal shift away from visiting malls, I’m not sure it’ll ever be possible to add 100 more Cheesecake locations in the U.S. It’s true that Cheesecake is in better malls and what I’ve seen anecdotally is the very best malls I’ve been to in New Jersey and Texas show no signs of any traffic decline while the very worst malls I’ve been …

I know you already published your WTW post-mortem post but I have been an intermittent reader and after WTW’s recent run, decided to check in on your blog.

I first heard about WTW as an investment thesis from your blog. I got the free sample of Avid Hog recommending WTW. I bought my first shares on 9/9/13 and in less than six months, my WTW position occupied 30% of my retirement portfolio. I proceeded to keep buying sporadically and even had the courage to pick up 300 more shares when it hit $6.18 on 5/26/15 – my only purchase of WTW that year. My holdings had an average purchase price of $24.52.

I believe in what WTW is about. Obesity is a systems problem. It is complex…I’m a pastor and I work with substance abuse addicts. Besides behavioral modification, a huge part of recovery is community support, peer reinforcement, and mindset change – all elements of what WTW groups do. Obesity has elements of addiction and disease. I view WTW as a kind of 12-step recovery for obesity. Because of the nature of obesity and addiction, WTW’s program will not be successful for even a majority of people but it will be successful for many. Oprah’s first ad was also incredible…

I sold 14% of my shares in November and December of 2015 after the Oprah announcement. I wanted to free up some capital for other purposes and re-coup some losses. I sold another 38% in gradual increments this year. I made a modest 5% total gain on all the sales (FIFO). I still have just under 50% of what I originally purchased, at a paper gain of 146%.

My total return (paper + actual) from 12/6/13 to 9/22/17 is 52.67%, besting the S&P500’s 38.53% rise for the same period.

I often felt terrible about pouring more money into WTW as I watched it decline in 2014 and 2015. It was rough. I kicked myself for not considering the impact of debt. I told my wife about my decision and she shook her head. Those were difficult times but I quickly learned not to base my mood off WTW swings. Many days, I would look at the stock price, shake my head, and just laugh. There was no rhyme or reason for the price changes.

I definitely hated your advice but was reassured that you had skin in the game. I also thought the market was undervaluing everything about the company. It was kind of ridiculous. I stopped reading your blog this past year and I’m glad I didn’t read about you selling. It might have influenced me to do the same.

Lessons learned:

1) I won’t make any company 30% of my portfolio again. WTW is currently 20% and I’m gradually taking that down.

2) I’ll take a company’s debt more seriously before jumping in.

3) Belief in the underlying premise of the company is what drove me not to sell completely. I had hope this company …

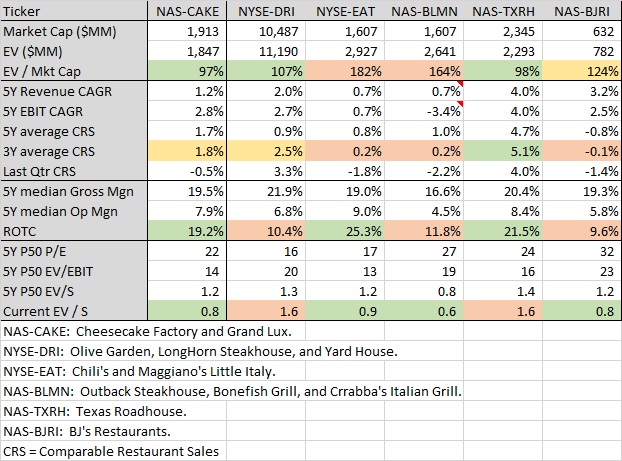

Someone who reads the blog emailed me about Cheesecake Factory (CAKE):

“Why are you not buying CAKE – it is around 66 cents on the dollar – at 40 dollars (a share)?”

When I answered that to his satisfaction, he asked:

“…So your options right now are most likely OMC, Howden and CAKE?You said in your OMC (stock report) that it was the best business you’ve ever analyzed. Is that still the case, especially compared to CAKE etc.?”

Omnicom is a better business than Cheesecake. However, Cheesecake may have more room to deploy capital within the business for the next 5, 10, 15 years. Apparently, Cheesecake management still thinks they can grow the concept from 200 locations to 300 locations. It’s not unheard of for them to open 8 new restaurants a year. So, that’s probably equivalent to 3% compound annual growth in the number of Cheesecake locations over a period of 10-15 years. Each location may be capable of earning a 10% to 15% after-tax return on the company’s cash investment of say $8 million to $12 million (they also sign a lease, but this does not tie up any shareholder money). Let’s call it $10 million per location in cash the company puts in and they can repeat that same $10 million bet at each of another 100 new locations – that’s $1 billion more in reinvestment done at rates of 10% plus.

To put this in perspective: Cheesecake may be able to re-invest 50% of its current market cap over the next 10 years at rates of return equal to or greater than 10% a year. It can also buy back its own stock. Both companies can do that and I expect both will do that aggressively. But, Cheesecake may have this additional opportunity to invest about 50% of its market cap over the next 10 years in the actual business at good rates of return. For Omnicom to reinvest 50% of its market cap on those same terms, there would need to be something in the $8 billion to $9 billion price range that will earn a year one 10% plus cash return on your investment.

I don’t see how Omnicom can find something like that. Right now, Omnicom can only compete with that kind of value creating capital allocation by buying back its own stock. Omnicom’s stock would have to stay cheap for a long time while the company gobbled up its own shares for OMC’s capital allocation to add as much value as Cheesecake’s capital allocation. So, Cheesecake may grow intrinsic value per share faster than Omnicom. Omnicom’s still the safer bet if you had to own one stock forever. But, if you have to own one stock for the next 10 years – I can’t promise that OMC has a way to deploy as much cash as profitably as Cheesecake might. Again, I stress might (CAKE needs to find good mall type locations to do this).

I have been reading all of Warren Buffett’s old partnership letters the past week or so. These letters are the letters he wrote to his Investors yearly (and then semi-annually) from 1957- 1970 before winding down his partnerships to eventually run Berkshire. I was inspired to do so because I have also been rereading The Snowball by Alice Schroeder’s for the past month, and it’s awesome how it takes you back to the beginning and goes year by year in Warren’s life as the snowball was building up and starting to roll downhill. There are a few books I re-read every year, and The Snowball is one of them. (Also on that list is Poor Charlies Almanack, another book I highly recommend.) The partnership letters are too long to embed in this post, but if you go to this link you should be able to pull them yourself:

Although Warren invests completely differently now, there are still a lot of takeaways you can pull for yourself from his writings. One thing I found interesting is on page 20 in his 1961 letter where Warren goes over his different types of Investment Categories. I’ll let him explain:

“The first section consists of generally undervalued securities (hereinafter called “generals”) where we have nothing to say about corporate policies and no timetable as to when the undervaluation may correct itself. Over the years, this has been our largest category of investment, and more money has been made here than in either of the other categories. We usually have fairly large positions (5% to 10% of our total assets) in each of five or six generals, with smaller positions in another ten or fifteen. Sometimes these work out very fast; many times they take years. It is difficult at the time of purchase to know any specific reason why they should appreciate in price. However, because of this lack of glamour or anything pending which might create immediate favorable market action, they are available at very cheap prices. A lot of value can be obtained for the price paid. This substantial excess of value creates a comfortable margin of safety in each transaction. This individual margin of safety, coupled with a diversity of commitments creates a most attractive package of safety and appreciation potential. Over the years our timing of purchases has been considerably better than our timing of sales. We do not go into these generals with the idea of getting the last nickel, but are usually quite content selling out at some intermediate level between our purchase price and what we regard as fair value to a private owner. The generals tend to behave market-wise very much in sympathy with the Dow. Just because something is cheap does not mean it is not going to go down. During abrupt downward movements in the market, this segment may very well go down percentage-wise just as much as the Dow. Over a period of …

A reminder: 40% of my portfolio is in Frost. It’s the stock I like best.

Someone wrote me to ask about Frost’s interest expense:

“Hi Geoff,

I have not read your report on Frost…but right now I am looking at the latest balance sheet and (am) very surprised…the average interest expense is…paltry…the cost of funding is 0.032%. That’s extremely low, almost free. Am I right on this calculation? Or is it a mistake?”

My response goes into way more arithmetic than anyone wants to read. But, if you want the full picture of how I personally value Frost – read on…

First of all, a bit more than half of Frost’s deposits are in accounts that pay pretty close to 0% interest because they provide a lot of services and these customers are not hunting for yield. Frost pays “credits” to reduce the fees customers are charged for banking services. I think when we wrote our report it was about 1.5% combined interest and non-interest expense. Frost generally has the lowest non-interest expense of a bank I know of. They’re always a little lower than Wells Fargo (WFC).

Anyway, I did the calculation for last year’s interest expense that you did using average interest bearing deposits and annual interest paid on those deposits (the information is in the 2016 10-K at EDGAR). They paid 0.03% on average in interest (3 basis points). Which is what you said. However, remember, the Fed Funds Rate started 2016 at 0.25% to 0.50%. So, the 2016 interest rate expense for any bank is very misleading.

In the long-run, I expect Frost to pay 0.5 times what the Federal Reserve pays for the same amount of money. So, if we end this year at say a 1.5% Fed Funds Rate and then it just stayed there, I’d expect Frost’s interest expense to rise to 0.75% eventually.

The formula:

FFR * 0.5 = Frost’s interest expense is pretty accurate.

That’s only the cash interest rate though.

On some accounts, Frost also pays an “earnings credit rate” that customers use to offset fees for services the bank would otherwise charge for. So, back in 2016, Frost might have been paying 0.03% on an account in cash interest but then 0.25% in credits you can use to offset bank fees.

Of course, it’s the total expense that matters for a bank. You have to count both the interest expense and the net non-interest expense when calculating cost of funds. Frost pays maybe 1.4% of deposits in net non-interest expense and then you have the interest expense.

So, the bank’s total economic cost of funding would really be:

FFR * 0.5 + 1.4% = Frost’s total cost of funding.

So, if we end 2017 at a 1.5% Fed Funds rate and the rate stayed there, Frost should be getting their money at about 0.75% (interest expense) + 1.40% (net non-interest expense) = 2.15%.

If the Fed Funds Rate was a more “normal” 3% to 4%, then Frost’s …

I like Cheesecake Factory (CAKE) a lot. There’s a write-up in the Focused Compounding member idea exchange about it. If I was to buy something right now, it would probably be CAKE. It’s a good business facing a temporary problem. Over the last two years, “food away from home” (at restaurants) is up 5% in price while “food at home” (supermarkets) is down 1.6% in price. So, the relative cost of eating out versus eating in has changed 6.6% in the last 2 years in the U.S. As economic theory would say has to happen, value seeking households have done some substituting from eating out to eating in. This has caused a decline in same store sales. The Cheesecake Factory’s same store sales are down 1% this year. The stock is down 32%. I had researched the business previously. CAKE shares were probably about fairly valued at the start of this year ($60 then vs. $40 today).

I would consider buying Omnicom (OMC) at about $65 a share. It’s at $73 a share now.

And you know I like Howden Joinery and continue to follow that stock as a possible purchase as well.

Not that long ago, I dropped everything and looked intensely at AutoZone (AZO) when it plunged just under $500. It’s at $570 now. I liked what I saw. At $500 a share, I think AutoZone would make sense as a “value” stock (really more of a cannibal that grows EPS through buybacks). But – for me at least – it’s the kind of stock you’d want to buy now and sell in 3 years or whenever its multiple expands again instead of holding forever.

I’ve looked at other companies recently, but have not bought any.

I looked at Howard Hughes (HHC) this past week. The company still owns a lot of valuable land in high-end master planned communities like Summerlin, Nevada (about 10 miles from the Vegas Strip) and is developing commercial real estate at the South Street Seaport in Manhattan and Ward Village (about 3 miles from Waikiki Beach in Honolulu). It has nice assets. It doesn’t seem obviously overpriced (before I looked, I expected it would be). But, I can’t prove it’s cheap. I’m only able to come up with estimates for some of HHC’s assets. Not all. I can’t imagine ever being able to come up with a solid appraisal value for the whole company.

I plan to look at Green Brick Partners (GRBK) and LGI Homes (LGIH) this week. They build homes here in Texas and elsewhere.

The only U.S. stocks that show up on Ben Graham type screens right now are a lot of retailers and some homebuilders. There’s literally nothing else here in the U.S. that’s quantitatively cheap anymore.…