Note: Sponsored ¼ share ADRs also trade under “PANDY” in U.S. Dollars

Pandora A/S is the largest jewelry maker in the world

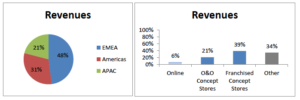

Overview Pandora is a vertically integrated jewelry maker that has rapidly grown from a local Danish Jeweler’s shop to the world’s largest jewelry manufacturer, producing more than 100 million pieces of jewelry in 2017. The original jeweler’s shop in Copenhagen, Denmark, was opened by goldsmith Per Enevoldsen and his wife Winnie in 1982. The company quickly transformed from a local shop, to a wholesale retailer, to a fully integrated global behemoth that designs, manufactures, directly distributes (in most markets), and retails its own jewelry. The company now sells in more than 100 countries through 7,800 points of sale. If you’ve ever been to a grade-A mall during Christmas or Valentine’s Day, you’ve probably witnessed the crazy lines snaking out of their small glass stores. Jewelry makers are segmented by price: Affordable (less than 1,500 USD), Luxury (1,500-10,000 USD) and High-End (greater than 10,000 USD). Pandora is in the affordable category by price but claims to have an ‘affordable-luxury’ brand. The company gets a little less than half (48%) its sales from EMEA (with 71% coming from UK, Italy, France, and Germany), about one-third (31%) from Americas (with 74% from US) and one-fifth (21%) from APAC (with 43% from Australia and 28% from China). The company’s sales are geographically diverse and in mature markets. To make it easy, let’s break down Pandora’s business model into two main retail formats:

1) Concept Stores (about one-third owned and operated by the company and two-thirds franchised): Concept stores are full-blown branded Pandora stores which only carry Pandora products and displays.

2) Other: other points of sale consist of “shop-in-shops” which are clearly defined spaces in other stores (think a little kiosk in an airport Duty-free) that only carry Pandora products and 3rd party distributors which can be either multi-branded retailers or non-branded retailers.

Pandora currently gets 66% of its sales from Concept Stores (plus online) and 34% from “other.”

We’ve discussed where the company sells and how they sell……..but What do they sell?

Pandora is the world leader in charms and charm bracelets. It’s their bread and butter. It’s estimated they own about 30% of the charm market and 75% of their revenues are generated from this category. Estimates are that charms and charm bracelets make up only 6% of the total jewelry market. In essence, Pandora sells you a bracelet for somewhere between $80-150 and then you fill the bracelet up with charms that are $50-150 each. Pandora sells 73 million charms per year (200,000 per day) and 14.5 million bracelets per year (40,000 per day). Pandora’s brand and leadership position in the charm niche is by far its most important asset.

Durability

The most prevalent risks to the durability of the company are a decline in the popularity of charm bracelets or a change in perception to the ‘quality’ of Pandora’s products. As mentioned in the

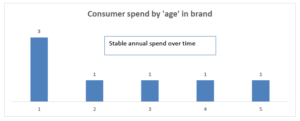

‘overview’ section, the majority of Pandora’s revenue comes from charms and charm bracelets. This is both good and bad from a durability standpoint. On the one hand, a major decline in the popularity of charm bracelets would obviously have a major impact on Pandora’s business. It would be very, very bad. This is a real risk. On the other hand, the charm bracelet model creates stable recurring revenues from the same customers year after year. The company tracks “consumer spend by age” which shows customers typically spend a large amount on their first purchase (about 3x more than their subsequent purchases because they’re buying the bracelet and more than one charm) but then has very stable recurring purchases in the subsequent years.

Pandora is focusing on diversifying their revenues in the next 5 years into other categories (rings, earrings, neckwear) so that their charms make up more like 50% of total revenues and the other is split between the rest. Will they be successful? No idea. They have been so far (their revenue split in 2012 was 90/10) but I have no opinion on their future here. Regardless, Pandora is a business that has needed to retain very, very little earnings to grow. They haven’t needed to invest in more assets due to their product economics and diversifying into these other categories is unlikely to change this. In terms of demand durability, jewelry is a durable industry. Women always have, and its logical to assume will always, wear jewelry. So the real question here is whether women will continue to want to wear charm bracelets. There is evidence that charm bracelets began appearing from 400-600 B.C and were worn by the Assyrians, Babylonians, Persians, and Hittites. Charms have gone through periods of popularity all around the world and in different time periods- all the way from the ancient Egyptians to Queen Victoria and the European noble class. Charms bracelets have been worn to symbolize and denote family origin, religion, faith, luck, etc. A charm bracelet is a small but essential piece of a woman’s jewelry wardrobe but like all things fashion, has historically waxed and waned. All fashion items have the risk of going out of trend for a period until they come back around. Pandora does have the ability to adapt to social trends by creating new charms through a quick life cycle process (goal of 4 months from conception to new product launch) but this doesn’t address the durability of the bracelets as an entire category. This is difficult to predict. Diamonds have withstood the test of time. Other jewelry trends haven’t. Why do women buy jewelry in the first place? 1. Status 2. Self-Expression 3. Aesthetic Why do men gift jewelry? 1. Status 2. To Express Care (men often think that the more luxurious the ‘status’ the brand reflects, the more they’re expressing care). So far, Pandora has managed not just to create reputation for being luxury and not just a reputation for being affordable, but ‘affordable-luxury.’ This is key to their continued success. We’ll discuss this more in the “Moat” section but for now, just understand that Pandora attracts both high income and lower income consumers. The income distribution between their consumers is: Low: 24% Mid-Low: 26% Mid-High: 25% High: 25%

While I’m not convinced Pandora’s products come with much of a ‘status’ like a Tiffany box, they check the boxes on Self-Expression, Aesthetic, and Expressing Care. Self-Expression: The entire concept of charms are predicated on self-expression. Each charm bracelet is different and unique to that individual. A female engineer from an island who just spent Christmas with her fiancé is going to have a palm tree, calculator, and Christmas tree on her wrist while a new mom who got married at Disney World is going to have ‘precious boy/girl’ charm and a Belle Dress on hers. You get the point. The CEO of Pandora talks about how if two women walk into a room with the exact same dress or high-end necklace, there is immediate tension. In contrast, when two women walk into a room and both have on Pandora bracelets, a conversation is struck. I believe this. I’ve seen it happen.

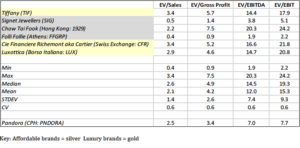

Aesthetic: The complexity of Pandora’s designs are more advanced than their competitors. Because the company is able to focus on this category and it’s a relatively small percentage of their competitors sales (none of the competitors separate out ‘charms’ as a separate category. Some don’t sell charms), Pandora has been able to invest in design innovation which has led to charms with more dimensionality and detailed craftsmanship. A look at the product offerings from Tiffany, Kay Jewelers (Signet), Folli Follie/Links of London, and Chow Tai Fook shows this. Cartier and Swarovski don’t sell charm bracelets. A look at the evolution of Pandora’s products over the years also depicts this point (see slide 81 of 2016 Capital Markets Day Presentation or slide 59 of their 2018 Capital Markets Day Presentation for more on this). Expressing Care: Gifting is one of the biggest appeals for the Pandora proposition. Approximately 43% of Pandora purchases are from male-gifters, 31% are from female gifters, and 26% are self-purchasers. Since Pandora is an affordable-luxury brand, gift recipients feel the butterflies when they get a Pandora gift while gift givers feel they’re getting bang for their buck at a high quality. Once the initial bracelet purchase is made, they also know they have a low cost, minimum effort gift idea for 1 out of every 4 special occasions (hypothetical) over the next 8 years to come. For the recipient, each charm is just as special as the one before because each item symbolizes a new and different aspect of their personality, a new memory they’ve created, etc. Self-expression doesn’t get old, it’s durable. Easy gifts are durable. Memories are durable. Are Pandora’s profits durable? Does it make sense to compete with Pandora in charms? For the luxury competitors, Tiffany does compete with Pandora in charms. However, this clearly isn’t Tiffany’s focus and Tiffany’s bracelets are priced between $485-$2,000. It doesn’t make sense for any luxury brand to compete with Pandora on price as this would be a self-inflicted wound. Luxury brands focus on selling small quantities at high prices. All of the affordable competitors compete with Pandora. There are 2 additional private affordable competitors (Alex & Ani and Thomas Sabo) but they are not significant. Both Folli Follie and Chow Tai price their charms at a lower price point and don’t have nearly the offering in terms of quantity or quality. Pandora’s closest competitor in terms of offering is Links of London, a fully owned subsidiary of Folli Follie, but they are much much smaller and at the end of the day, Pandora has no true peer. Are the returns durable? Based on its industry position, the company is substantially more insulated to withstand an economic downturn than their luxury competitors. Pricey brands like Tiffany and Cartier see a significant sales decline during recessions. Although Pandora hasn’t been a public company through one of these cycles yet, we can look at an affordable-luxury company like Luxottica, with sunglass prices around the same as a Pandora bracelet, to see that they had a higher resilience during the crisis than the companies with pricier items (granted- a good chunk of Luxottica’s sales come from prescription eyewear also). Consumers still gift during recessions, they just gift more affordable goods.

The company has an asset light business and you’ll see their working capital diligence later on. Pandora’s growth has slowed substantially in the last year as its transformed into a more mature company. The company has also suffered somewhat from a decline in US mall traffic. One might wonder if the company will need to start investing in more assets to grow the business. Probably. However, Pandora does not acquire other companies and doesn’t appear to be interested in reinventing the wheel by offering products that aren’t complimentary. Instead, they plan to execute 3 initiatives:

1) acquiring successful Pandora franchises and distributors. In 2017, Pandora owned 35% of its Concept Stores and 65% were still franchised. In the next 5 years, Pandora plans to take over 70-150 franchise stores per year and increase their ownership to 66%. According to management, owned stores generate double the revenue and 1.8x EBITDA.

2) maintain leadership position in charms through product innovation and marketing

3) cross-sell ring, neckwear, and rings

A decline in the popularity of charm bracelets would hurt Pandora a lot. They invest a lot in marketing to maintain their brand image and awareness. They control their brand all the way from production to retail. Because they are fully vertically integrated, if the brand declines in popularity, it would have to be a self-inflicted wound. Pandora has almost as much control over their brand as Luxottica has over Ray Ban and Oakley. If charm bracelets are here to stay, Pandora is here to stay. Pandora is the Amazon of the charm jewelry segment.

Moat

According to the company, the Pandora brand became the number 1 most recognized jewelry brand in the world for the first time in 2017, with 83% recognition. The runner-ups, in order, were Swarovski (80%), Tiffany (71%), and Cartier (63%). In 2010, their brand recognition was only 36%. Marketing is very important for a company like Pandora. They spend 10% of total revenues per year on marketing. They have partnerships with Disney and celebrities like Ciara advertising their latest collections.

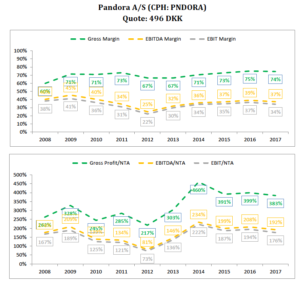

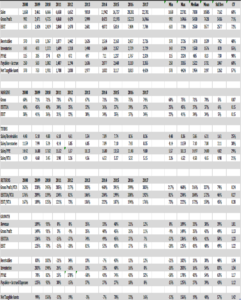

Pandora’s gross margins are extremely high, especially for a company with a lot of stores and high growth over the last 10 years. Their 5-yr average gross margin is 72%. For the luxury competitors (Cartier’s, Tiffany, and Luxottica), the average gross margins are around 64%. For the affordable competitors (Signet, Chow Tai, and Folli Follie), they are around 36%. What about EBIT margins? Pandora = 5-yr average 34% (even though management expects this to drop to 32% between 2018-2022). Luxury competitors = 16%. Affordable competitors = 13%. Pandora has 12% higher gross margins than luxury competitors and 100% higher than affordable competitors. Pandora has double the EBIT margins of both. What does this mean? It means that Pandora has pricing power. It’s an indication that they may indeed have established an ‘affordable-luxury’ brand. Let’s look at inventory turnover. Pandora turns over their inventory 2 times per year. The turnover of the pricier luxury brands

(Cartier, Swarovski, Tiffany ) is expected to be lower but the turnover for the affordable competitors- Signet, Chow Tai, and Folli Follie is 0.4, 0.5, and 1.3 times per year. Luxottica has better turnover in the mid to high 3s but Luxottica sells small volumes of sunglasses for premium prices. Pandora sells large volumes for premium prices. If Pandora were to increase the price of all charms by, let’s say, $2.50, and all bracelets by $5.00 (assuming same sales volumes- although it’s probably a little tricky to increase too much and maintain their brand ‘affordability’), revenue would increase 6.5%. Pandora has scale. It is the largest jewelry maker in the world with 5x the capacity of any other. Its 2017 shipped volume was 117 million and is expected to ramp to 200 million over the next 5 years. It has 2 large manufacturing facilities in Thailand that employ 13,200 manufacturing jobs. That’s a lot of manufacturing jobs. As stated earlier, its products have evolved in complexity through the years. For example, in 2012, the company set 230 million stones in their charms whereas in 2017, 2.6 billion stones were set. Scale like this comes with a modest amount of intellectual capital between the design and manufacturing. Between the brand advantage and scale, it will be extremely difficult for any of the smaller, affordable competitors to compete. Signet is the only affordable competitor that is larger than Pandora (both by market cap and sales), but Signet’s focus is on diamonds. They are the largest diamond retailer in the world. Signet owns Kay Jeweler’s and Jared’s and it would be hard for them to compete in the charm segment. Signet has recognized this and some of Pandora’s “other” retail formats are actually Jared stores (or website) where Pandora charms are sold. I’ve discussed in the ‘durability’ section why it doesn’t make much sense for the luxury brands to compete with Pandora on price. In terms of the luxury jewelers that I’ve evaluated, they seem to play friendly for the most part. The industry as a whole has rather good returns on capital and several niches have been established. For example, Tiffany focuses on diamonds and engagement rings while Swarovski focuses on costume jewelry and anything crystal. Cartier, Bvlgari, and some of the others seem to market to the higher end of the price scale. Pandora is fortunate the niche they stumbled upon has a wider customer base than the rest-luxury for the middle class. The industry appears, so far, to have some Nash Equilibrium-ness to it.

Quality

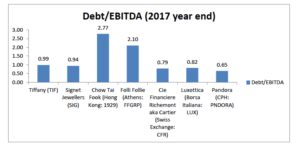

Pandora has earned very high returns on its net tangible assets even while growing Sales and EBIT at a CAGR of 20%+. The company’s growth is slowing down and management expects 7-10% sales growth from 2018-2022 but their returns on tangible assets should continue to remain strong as long as the company continues to diligently manage working capital the same way that they have for the last 10 years. In the last 10 years, their lowest EBIT/NTA by far was 73%. All other years were over 100%. I don’t want to get stuck on any specific numbers but like to look at this more qualitatively. The return would be more than adequate even if it dropped by 75%. This is a high quality business. Pandora’s EPS can almost be treated as true free cash flow. Two-thirds can be sustainably paid out and a third reinvested at very high rates of return. In 2013, the company had a net cash position (Net Debt/EBITDA of -0.2) and was paying out (in dividends + buybacks) 64% of its after-tax earnings. At this point, the company made a decision to finance its growth through leverage (to a range more in-line with the industry) and begin distributing all of its after-tax earnings. Over the next 4 years, from 2014-2017, Pandora, on average, distributed more than 100% of its after-tax earnings to shareholders while growing a lot. The company’s Net Debt/EBITDA at the end of 2017 was 0.6 but their total debt to EBITDA was still lower than all of their competitors.

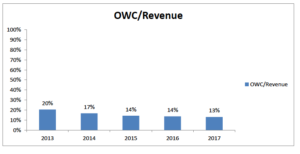

First let’s look at the yield if Pandora chose not to increase leverage. At 496 DKK/share, Pandora trades at 8x EBIT which I estimate to be a price to free cash flow of about 13, thus, Pandora could return about 8% of shareholders purchase price if it used all earnings to buy stock at this level. Without increasing leverage, I estimate Pandora can pay out around 65% of its after-tax earnings through a combination of buybacks and dividends while growing sales by 7-10% a year and earnings by half of sales. Historically, earnings have grown faster than sales but management expects margins to drop a couple points in the next few years. So we’d have about 5% (.65 x .077) of dividends+buybacks plus 3.5% earnings growth (assuming 7% sales growth) minus 1% option dilution. That’s a 7.5% return or better while you hold the stock. If Pandora grows sales 9-10%, the stock could return 9% a year. Now let’s look at the return as Pandora continues using leverage. The corporation will likely continue financing growth for the next year or two with debt, as management has communicated they expect to distribute around 6 Billion DKK in 2018 (all of after-tax earnings, or more). The company has a policy to keep Net Debt/EBITDA under 1 which means that in the future, as they approach this number, they will need to retain more earnings and subsequently distribute less. Assuming 5.8B is distributed, which is just slightly more than their 2017 distribution and under management’s guidance. Yield = 10% + 3.5% – 1% = 12.5%. In conclusion, the stock may return around 12% over the next 2 years and 7% thereafter. If the company was in a steady state and no longer growing, it could return almost all of its after-tax earnings, giving a yield virtually equivalent to its E/P ratio. The management team has done an excellent job over the years tying up less and less shareholders money in “operating working capital,” defined as Inventory+ Receivables- Payables. See below.

Look for continued vigilance here.

Capital Allocation

Pandora is going to allocate capital as follows:

1. Maintain debt under 1x Net Debt/EBITDA .

2. Buying franchises, distributors, and opening new concept stores.

3. Improving manufacturing/R&D capabilities.

4. Shutting down unbranded points of sale (Pandora is aiming for more and more direct control. From 2013-2017, their total points of sale have decreased from 10,279 while their total concept stores have gone from 1,100 to 2,446).

5. Remainder paid out as dividends+buybacks.

The only thing worth mentioning here is that Pandora’s cash distribution in 2017 was about 5.7B, consisting of 4B in dividends and 1.7B in buybacks. In late 2017 and early 2018 the share price had dropped from a 2017 high of 900/share to levels around 580-600/share. Based on the drop, the Board communicated in 2018 their cash distribution would constitute 4B for buybacks and 2B for dividends. In summary, they were price sensitive in the decision to repurchase shares vs distribute cash as a dividend. The management team has been shareholder friendly and good capital allocators thus far.

Value

Pandora is trading below a normal business price (EV/EBITDA of 8) and is a better than normal business. Due to a weak Q1 2018, Pandora’s stock has sold off and gone from 690 DKK to 495 DKK in the last 2 weeks. Its multiples contracted substantially and EV/EBIT went from 10.7x to where it stands today. Pandora’s closest peers in the jewelry industry are Chow Tai Fook (to a lesser extent) and Folli Follie, but the company is by far the largest charm/charm bracelet producer and far superior in quality to either. Luxottica has a similarly vertically integrated business model and sells premium products, but not in the same space. Tiffany and Cartier focus on much more expensive luxury jewelry and Signet targets the mid-market diamond market. Pandora is most like Luxottica with its returns on assets, most like Tiffany with its brand strength in the industry, and most like Folli Follie in terms of product offering.

Pandora:

Market Share: 2% of Jewelry Market. 30% of Charm Market. 5x next largest manufacturer. Location: EMEA- 48% Americas- 31% APAC- 21%. Mostly from mature markets.

Sales Growth (2018-2022): 7-10% Earnings Growth (2018-2022): 3-5%

Returns on Tangible Assets: 100%+ Return on Assets: 35%

Safety: Safe. Debt/EBITDA = 0.8

Quality of Earnings: Medium-High

EV/EBIT: 7.7

Luxottica:

Market Share: Almost all of Premium and Prescription Eyewear

Location: EMEA- 21% Americas- 57% APAC- 13%. Mostly from mature markets.

Sales Growth (2018-2022): 2-4% Earnings Growth (2018-2022): 6-8%

Returns on Tangible Assets: 70%+ Return on Assets: 8%

Safety: Very safe. Debt/EBITDA = 0.8

Quality of Earnings: High

Qualitative Advantages/Disadvantages: Way bigger than anyone else in both sunglass and prescription eyewear. Less cyclical.

EV/EBIT: 20.8

Tiffany:

Market Share: 2% of Jewelry Market.

Location: EMEA- 11% Americas- 45% APAC- 41%

Sales Growth (2018-2022): 5-7% Earnings Growth (2018-2022): 8-10%

Returns on Tangible Assets: 20%+ Return on Assets: 8%

Safety: Safe. Debt/EBITDA = 1

Quality of Earnings: Medium-High

Qualitative Advantages/Disadvantages: High durability. More cyclical.

EV/EBIT: 17.9

Folli Follie:

Market Share: 0.5% Jewelry Market.

Location: APAC (mostly China and Japan)- 68% Greece- 22% Rest of Europe- 9% N. America- 1% Sales Growth (2018-2022): 6-8% Earnings Growth (2018-2022): 6-8%

Returns on Tangible Assets: 20% Return on Assets: 8%

Safety: Possibly a fraud. If financials are real, Very safe. Price/NCAV = 0.33

Quality of Earnings: Very low

Qualitative Advantages/Disadvantages: No distinguishable moat (maybe some brand strength in China/Japan?). Extremely high working capital/revenue.

EV/EBIT: 2.2

Conclusion:

Luxottica has a better market position and higher quality of earnings, thus deserving of a higher multiple. Tiffany is more durable (although they’re currently facing some negative societal forces), stronger in the US, and will likely grow their earnings faster in the next 5 years. They also have slightly more debt, worse capital allocation and returns on capital, and likely more exposure to economic downturns. Pandora has advantage with its recurring revenue model and lack of competition in the charm niche. I think both companies are equally attractive when priced at the same multiple. However, Tiffany, and all luxury competitors, are trading at more than twice the multiple of Pandora. Both companies are higher quality than your average business and worth about 13 times EBIT. This means that Tiffany is over-valued right now at 18x EBIT while Pandora is undervalued at 8x. Both are good stocks to hold forever if you can buy them at a normal business price. Folli Follie is extraordinarily cheap (a net-net) but has extremely high working capital needs and may potentially be a fraud. If Folli Follie could ever reduce its working capital needs and turn earnings into true free cash flow, they could be a better stock pick. But right now they are a low quality company who has never distributed a dividend, doesn’t consistently buy back shares, is focused on reinvesting all its resources until they become a “global brand,” and has recently gotten caught up in a nasty battle with hedge fund QCM who released a short report alleging fraud.

Growth

The future growth of Pandora’s earnings per share is difficult to predict but I think it can grow at around half its sales growth. Improved operating leverage as Pandora opens more concept stores and converts franchises to owned and operated stores could improve earnings growth.

Due to Pandora’s recurring revenue model and heavy reliance on gifting, they have good opportunities to get customers back in stores (or looking on their website) and cross-selling some of their ring, earrings, and neckwear categories. The company has found that 30% of new consumers in charms move on to buy products in one of these other categories while 50% of new consumers in the other categories move on to buy a charm bracelet.

Jewelry is not a consolidated industry and the majority of the market is still made up of small local jewelers. Because of this, the branded jewelry industry is expected to grow at a CAGR of 6% over the next 5 years, following in the footsteps of general retail over the past 10 years as large multinational brands have taken market-share from local shops. This trend has already started and is expected to continue. Emerging markets are a big opportunity for jewelry companies. India and China are estimated to be the largest markets in the world. Pandora has recently entered China and has been growing rapidly. They also opened their first store in India last year.

Pandora estimates that they have the largest market share in Australia, U.K, and Italy, with 12%, 11%, and 11% respectively. In the U.S, China, and India, the three largest markets in the world, their share is 2% or less. Even in the charm segment, where Pandora dominates, the companies only makes up 30% of the global market. In summary, there seems to be plenty of headway.

Misjudgment

The biggest risk of misjudging the company’s prospects is betting on the fact that charm bracelets are here to stay. The second biggest risk is that there is only 10 years of data and thus we haven’t been able to observe performance during a full economic cycle, thus making reliability difficult to determine.

I won’t discuss these two points much more since I’ve already touched on both in the durability section. In terms of charm bracelets, they’ve become a staple item in women’s jewelry boxes. They’re a way to express multiple facets of their self by wearing one piece of jewelry. The second is a real risk that must be accepted. The company has been around for 30 years but only public for 10. We cannot know the performance during a full economic cycle, but can take a look at competitors during cycles. This still isn’t the best approach since Pandora is really the only affordable-luxury brand of those mentioned and more reliant on gifting than other products. All companies struggle during recessions and economic downturns, but we wouldn’t expect Pandora to struggle any worse than their competitors. In fact, because of their position, it would be expected the company would be more insulated than some of the luxury brands.