Parkit Enterprise: Activist Controlled Parking Lot Owner Looking to Monetize Holdings, Trading at a Discount to Net Asset Value

WRITE-UP BY THOMAS NIEL

(Image Created by the Author; Data via Parkit Investor Relations Page and Author’s Calculations)

(Image Created by the Author; Data via Parkit Investor Relations Page and Author’s Calculations)

Parkit Enterprise is a Canadian-domiciled owner of parking lots in the United States.

Investors have forgotten about Parkit, pushing the stock to trade well below its underlying value.

But one investor saw opportunity and has taken the reins to realize the company’s underlying value. Leonite Capital, a family office led by Avi Geller, has acquired a large position, and last year took control of the board.

Following this proxy-fight win, Leonite is looking to extract full value out of the company. But can they achieve what its prior management presumably failed to accomplish? Will realization of full value occur within an attractive timeframe (2-3 years?).

Let’s take at Parkit and see if the current discount to NAV is justified or presents a strong investment opportunity.

Background

Parkit Enterprise, Inc. (TSX.V: PKT; OTCQX: PKTEF) is a Canadian-domiciled owner of parking lots in Colorado, Connecticut, and Tennessee. The stock trades on the Toronto Venture Exchange, as well on the US OTC markets.

Parkit started out as Greenscape Capital Group, a holding company engaged in various “green”-related businesses. After developing the Canopy Airport parking facility, the company decided to sell off its non-core holdings and focus entirely on parking.

The company renamed itself Parkit Enterprise in 2013. Starting in the mid 2010s, Parkit formed a partnership with parking lot management company Propark America to acquire additional properties.

This resulted in Parkit becoming a major investor in two partnerships:

- OP Holdings JV, LLC. This partnership was formed in 2015 with Och-Ziff Real Estate as the primary investor. In 2015, OP acquired Parkit’s Colorado property, as well as properties in California, Connecticut, and Florida.

- PAVe Nashville, LLC. a 50/50 partnership with Propark. This vehicle acquired an airport parking facility in Nashville, TN in 2015.

This opaque ownership structure is part of the reason why investors have overlooked Parkit. Like with other similar vehicles (such as Regency Affiliates), there is the added risk of being a “passive investor in a passive investment”.

OP Holdings JV

The bulk of Parkit’s investments are held through OP Holdings JV, a partnership with Och-Ziff Real Estate and Propark formed in 2015.

Parkit owns an 82.83% interest in Parking Acquisition Ventures, LLC (PAVe). Due to the success of two divestitures, Parkit has fulfilled the 15% IRR hurdle due to Och-Ziff. As per the terms of the operating agreement, proceeds from asset sales will now begin to flow to PAVe.

As per the operating agreement, PAVe is now entitled to distributions until it realizes a 15% IRR on its initial capital contributions.

Through OP, Parkit holds interests in 4 properties:

- Canopy Airport Parking Facility (nearby Denver International Airport)

- Riccio Lot Hospital Parking (New Haven, CT)

- Chapel Square Lot (New Haven, CT)

- Z-Parking (East Granby, CT)

Canopy Airport Parking Facility

(Source: Parkit Investor Presentation, April 2019)

(Source: Parkit Investor Presentation, April 2019)

The Canopy Airport parking facility was developed by Parkit in 2010, and was sold to the joint venture in 2015.

- 2018 NOI of $3.1m USD

- Appraised for $37.6m in 2017 in conjunction with a refinancing

New Haven, CT Properties (Riccio Lot, Chapel Square)

Parkit’s two New Haven properties (Riccio Lot hospital parking, and the Chapel Square lot) generate $274,000 and $371,000 in NOI, respectively.

(Source: Parkit Investor Presentation, April 2019)

(Source: Parkit Investor Presentation, April 2019)

Riccio was acquired for $4.3m in 2015. Chapel Square was acquired for $10.5m the same year.

(Source: Parkit Investor Presentation, April 2019)

(Source: Parkit Investor Presentation, April 2019)

Currently, both properties are assessed at valuations close the purchase price ($4.5m and $10.5m).

Z-Parking (East Granby, CT)

(Source: Parkit Investor Presentation, April 2019)

(Source: Parkit Investor Presentation, April 2019)

Z-Parking generates $258,000 in NOI. Acquired for $4m in 2015, the property is currently assessed for $3.5m

PAVe Nashville

Nashville Fly-Away (Nashville, TN)

(Source: Parkit Investor Presentation, April 2019)

(Source: Parkit Investor Presentation, April 2019)

- 2018 NOI of $429,000.

- Acquired in a partnership with Propark in 2015

- Parkit owns a 50% interest in the property.

- Acquired for $7.8m in 2015, the property in 2017 was appraised for $7.85m (cap rate approach) and $8.89m (sales comp approach).

Leonite Capital

Leonite Capital, a family office managed by Avi Geller, acquired a significant stake in Parkit in 2018.

A Leonite-led investor group went activist, lobbying for 2 board seats. The investor group won the seats, and quickly assumed negative control of the company.

In October 2018, Geller was appointed interim CEO. In late 2018, Parkit expanded their capital base via a rights offering. Leonite Capital, along with two other large shareholders (KDI Corporation Ltd. and B&M Miller Equity Holdings) led the offering, acquiring ~$700,000 in units.

Divesitures

In 2018, Parkit’s OP Holdings JV affiliate sold two parking lot properties:

- Expresso Airport Parking (Oakland, CA): Sold for $36.1m, achieving an IRR for equity investors of 42%.

- Terra Park Parking Facility (Jacksonville, FL): Sold for $6.8m plus $0.7m in deferred proceeds. This holding achieved a 24% IRR for the joint venture.

Because of the returns realized from these two properties, OP Holdings JV has satisfied its 15% IRR hurdle with Och-Ziff. As a result, proceeds from additional OP Holdings JV divestitures start flowing to PAVe.

Valuation

The primary valuation assumption is that Parkit’s current shareholder composition (Leonite, et al) wants to liquidate the portfolio and realizing the company’s underlying value.

To estimate what the net proceeds of Parkit’s investments through PAVe, let’s take a property-by-property look:

OP Holdings JV Properties

Canopy Airport

Parkit believes the Canopy property is worth approximately its 2017 refinancing appraisal ($37.6m).

This valuation is in line with its 2018 NOI ($3.1m), but there is one large caveat: Canopy does not own the underlying land beneath the parking lot. The current lease expires in 2035. According to this thread on the CoBF forum, PAVe is working to extend this lease to make the property more salable.

An implied 8% cap rate at the $37.6m valuation seems reasonable, but an additional discount may be warranted given the lease situation. I am discounting this valuation by 10%, bumping it down to ~$33.8m.

Chapel Square

OP bought Chapel Square for $10.5m in 2015. The parking lot facility is located underneath a large hotel in Downtown New Haven. Based on New Haven property records, the parking facility owns the underlying land along with the structure. They assess the property at ~$7.4m.

The $10.5m valuation is understandable given the projected revenues of Chapel Square. According to the OP Operating Agreement, Chapel Square was projected to generate ~$750,000 in NOI. Decline in net revenue has hammered the property’s operating income.

Considering this decline in income, and the need to turnaround this property, I believe the $7.4m valuation is a more realistic short-term valuation.

Riccio Lot

The Riccio Lot in New Haven, CT is assessed by Parkit at $4.5m. With 2018 NOI of $274,000, this implies a ~6% cap rate.

Assuming that 7% cap rate is the most reasonable valuation for this property, I believe the Riccio Lot is worth (at most) $4m.

Z-Parking

Z-Parking in East Granby, CT (adjacent to Hartford’s Bradley International Airport) is assessed at $3.5m. The property generates ~$258,000 in NOI. This is in line with reasonable cap rates for parking properties, and again I agree with Parkit’s valuation.

Parkit’s Interest in OP Holdings JV

Using current appraisals, properties are worth as follows:

- Canopy: $33.8m

- Chapel Square: $7.4m

- Riccio: $4.m

- Z Park: 3.5m

This generates total proceeds of $48.7m. After closing costs and outstanding debt, this leaves $16m in net proceeds.

Distribution of sale proceeds is your typical “Waterfall Model”. Per the OP Holdings JV Operating Agreement, Och-Ziff was entitled to asset sale proceeds up to a 15% IRR hurdle. Now that this hurdle has been satisfied, PAVe is entitled to distribution until it reaches a 15% IRR. Parkit receives 82.8% of these distributions.

If a sale closes about a year from now (July 2020), based on Parkit’s December 2018 investor presentation, PAVe will receive $14.5m in proceeds to satisfy its 15% IRR hurdle.

The next $3m in proceeds following this flow to PAVe. This amount however is split 40.6/59.4 between Parkit and PAVe’s other members. With only $1.5m left, this means the partnership does not reach either the promote tiers or the additional IRR handles (17%, 22%).

With Parkit due 82.83% of the IRR hurdle ($12m), and 40.6% of the next tier of distributions ($609,000), a conservative estimate of Parkit’s interest in OP Holdings JV is ~$12.6m.

Current Valuation of Nashville Property

Parkit’s Nashville holding (50/50 with ProPark) receives a frothy valuation in the investor presentation. But with just $429,000 in 2018 NOI, I am not confident in an $8m valuation.

Assuming a 7% cap rate, the Nashville property is likely worth ~$6.1m. With a 6% cap rate, $7.1m. Parkit’s valuation assumes the property’s income generation will return to levels seen when purchased.

To be conservative, $7m is a reasonable valuation for the property. Based on land comps (via Loopnet), I am doubtful that the land (5 acres) is worth more as a development parcel than as off-airport parking.

Subtracting closing costs and outstanding debt, Parkit’s 50% interest may only be worth ~$500,000.

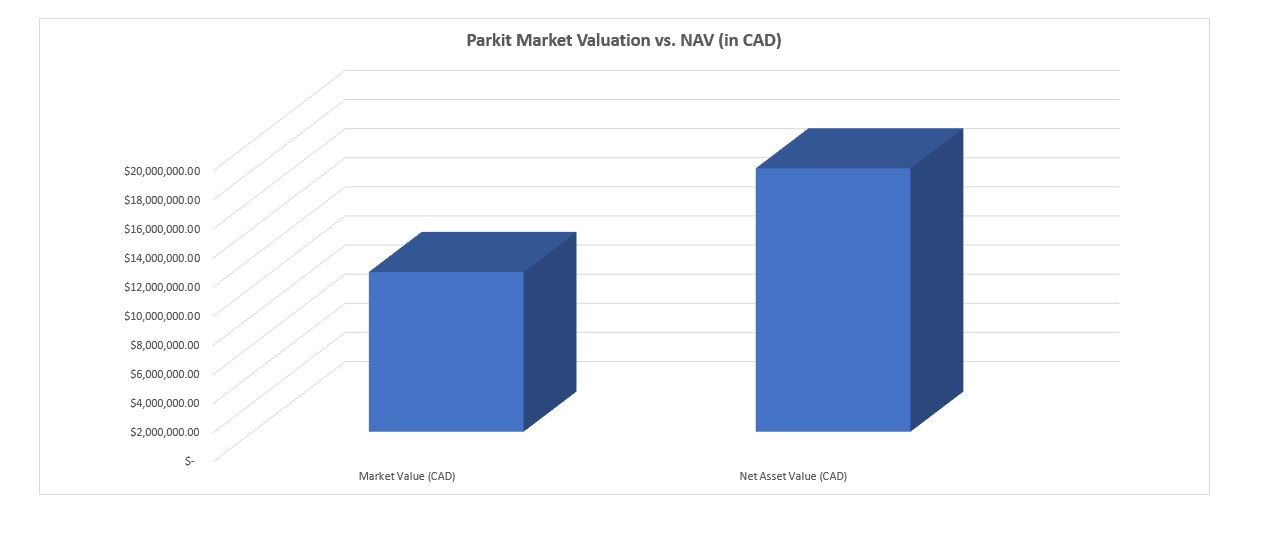

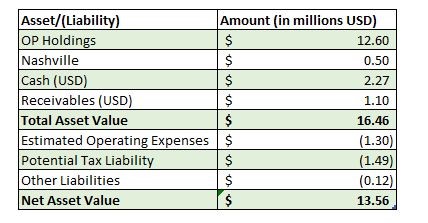

Conservative Sum-of-the-Parts

Calculations by the Author

To estimate a reasonable valuation for Parkit, I added up my assessment of the OP Holdings and Nashville investments, plus current assets on the balance sheet (figures taken from most recent financial filing). This gives us a total of ~$16.4m USD.

Subtracting out the on-the-books tax liability (see more below), payables, and an estimate of 12 months of operating expenses ($1.3m), we get a net asset value of ~$13.56m USD.

This converts to ~$18.1m CAD. With ~34.85m outstanding shares, PKT is worth ~$0.52 CAD/share, a 62% premium to the company’s current trading price on the Toronto Venture Exchange.

Optionality of Upside

Based on how the Parkit situation plays out over the next 2-4 years, the net value of Parkit shares may be substantially higher than this amount.

Taking a look at the potential scenarios presented in the April 2019 investor presentation, a liquidation of the assets in 2021 or 2023 would generate a greater net asset value for Parkit. This is primarily due to Parkit (via PAVe) being entitled to a 15% IRR before promotes and additional IRR hurdles are paid out.

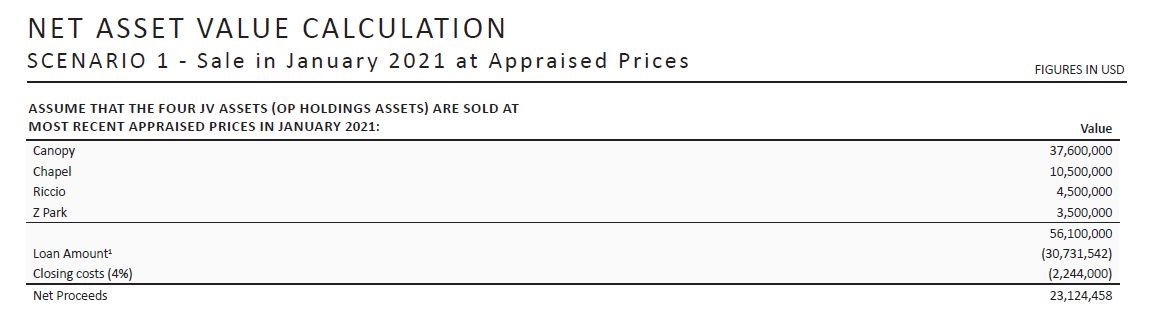

For example, let’s take a look at Parkit’s January 2021 estimate of the company’s liquidation value:

(Source: Parkit April 2019 Investor Presentation)

(Source: Parkit April 2019 Investor Presentation)

Note that in all of Parkit’s calculations, they assume the properties could be sold for the 2017 appraised values. Given this is ~18 months out, it is possible that Chapel Square could be stabilized to justify a valuation around the original purchase price.

The Canopy situation (extension of land lease) could also be resolved at this point, allowing for disposal at the $37.6m valuation.

With the OP realizing $23.1m in net proceeds, the waterfall distribution would be as follows:

(Source: Parkit April 2019 Investor Presentation)

Thanks to the 15% IRR handle, PAVe (82.83% owned by Parkit) receives a large share ($15m). As seen in my conservative valuation, the next $3m goes to PAVe as an incentive, with most of these proceeds flowing to the ProPark affiliate that manages PAVe (Parkit only receives 40.6%).

After this comes the first “promote”, split 50/50 between Parkit and Propark. After this comes an additional IRR hurdle of 17%. As seen in the JV agreement, Och-Ziff participates at this level of the waterfall.

Flowing all the way down to the 22% IRR hurdle, PAVe receives total distributions of $20.2m. Based on the terms of the PAVe operating agreement, Parkit receives 82.83% of the IRR hurdle distributions, 40% of the $3m incentive, and 50% of the various tiers of promote.

These add up to $15.1m. If the separate Nashville property can be sold for $8m (Parkit’s assumed valuation), this would yield the company an additional ~$1m in proceeds net of debt and closing costs.

On page 22 of the Parkit investor presentation, you can see Parkit’s estimates on how the rest of net asset valuation can be calculated. This includes their estimates of operating expenses through January 2021, as well as additional tax liabilities.

In this estimate, Parkit believes the company’s net asset value in January 2021 could be $17.5m USD ($23.1m CAD), or ~$0.66 CAD/share. Fully diluted valuation (inclusive of the 1.84m in options) is approximately $0.65 CAD/share.

This is more than double the current trading price.

The Longer The Delay, The Greater The Flow to Parkit

Because of the 15% IRR hurdle, Parkit’s initial investment continues to grow at a 15% clip before other partners are entitled to additional distributions. Because Och-Ziff has already realized their 15% hurdle, they are not entitled to additional upside until PAVe receives its preferred return.

This creates an incentive to Parkit to delay the sale of the properties until they can sell them at these assumed valuations.

For example, using the same estimates in Scenario 1 ($23.1m in net proceeds for OP Holdings), PAVe receives a much larger chunk:

(Source: Parkit April 2019 Investor Presentation).

(Source: Parkit April 2019 Investor Presentation).

In this scenario, PAVe is entitled to the first $19.1m in proceeds, with the $3m incentive eating much most of the remainder.

With this incentive on the part of Parkit/PAVe, there is definitely a conflict between them and Och-Ziff. If the joint venture were able to liquidate today for the $23.1m in net proceeds, Och-Ziff would receive a materially larger share.

Catalysts

Sale of Parking Assets As Development Sites

In a promotional video interview with Proactive Investors, Parkit Chairman David Delaney discussed two interesting angles relating to Parkit.

The first is the opportunity to sell parking facilities as development sites. Delaney talks up this opportunity. He mentions that Parkit’s two divestitures (Oakland and Jacksonville) were sold to owners looking to redevelop the sites.

To counter this management commentary with investor skepticism, it is apparent that Jacksonville and Oakland (the two sold properties) were the more attractive redevelopment sites.

In the case of Canopy, OP Holdings does not own the underlying land. With the New Haven Properties, they are either too small (Riccio) or already built upon (Chapel Square) to be sold for redevelopment. Based on Loopnet comps for commercial land in East Granby, CT and Nashville, TN, their current valuations are driven more on their profitability as parking lots as opposed to redevelopment.

Perhaps future Parkit investments will target properties similar to Jacksonville and Oakland, but in the near term this is not a strong catalyst.

Slow Liquidation within 3-5 Years

Under Avi Lerner/Leonite’s management, Parkit is pursuing monetization of the parking investments made in 2015. They may pursue further investments with ProPark/PAVe, but realizing this intrinsic value is priority number one.

Parkit’s investor presentation implies management is interested in selling the PAVe interests between 2021 and 2023. Based on PAVe’s preferred IRR of 15%, this will continue to grow Parkit’s book value even if a sale is delayed.

Parkit believes after-tax value of its assets in 2021 and 2023 will be ~$0.65 CAD/share and ~$0.71 CAD/share, respectively.

Of course, by 2023 it may prove difficult to unload these properties. While Parkit’s investing thesis regarding parking lots are built on them being “rate reset proxies” (see more below), it is a risk to assume their lots will sell at ~7% cap rates.

New Investments with Targeted IRR of 15%

With Parkit winding down OP Holdings JV, the company is no longer beholden to the interests of Och-Ziff. It can now focus on acquiring parking lot properties in tandem with Propark.

Leveraging Propark’s expertise, Parkit can find new investments that with a strong targeted IRR (~15%).

It is debatable whether Parkit’s investors are interested in continuing this partnership with Propark. The current crop of major shareholders (Leonite, et al) are in Parkit to close the spread between trading price and intrinsic value. They are not parking lot investors pe se, although Leonite is active in commercial real estate.

Risks

For additional color commentary on Parkit, I would recommend this thread on CoBF. Forum members bring up several key risk factors:

- Operating performance of Canopy has waned in recent years

- Canopy sale may not be pursued until current land lease (expires 2035) is extended.

- Complex rights offering (limited to Canadian shareholders, but Leonite was able to participate via a private placement) appears dilutive to outsiders

- Concerns over realistic valuation of Nashville facility

Here is further information on these key risk factors:

Liquidation Takes Longer Than Projected

OP Holdings JV found suitors for its more attractive properties. What remains are the “problem child” holdings. Canopy faces stiff competition from other facilities adjacent to Denver International Airport. The Connecticut properties appear highly mature, and will likely sell at higher cap rates. The assessment for the Nashville property also appears inflated relative to NOI.

If it does take several years to unwind this myriad of holdings, Parkit (through PAVe) may benefit thanks to their preferred return of 15%. As long as their interest accrues 15% a year, they will receive the lion’s share of PAVe’s proceeds.

On the other hand, these investments could be a hot potato. With an anticipated recession yet to hit as of mid-2019, it appears certain that the real estate environment of the early 2020s will be more challenging than today.

.

Diversification From Parking Assets

With any idea built on “sum of the parts” as the primary catalyst, there should be a countering risk of “what will they do with the money”?

If Parkit were able to sell their holdings today, would they distribute the money in a liquidating dividend, or reinvest the proceeds? Corporate liquidations can be disappointing. Delays and additional costs can hammer down returns far below expected returns.

This could result in Leonite and the other large investors keeping the proceeds within Parkit, then using the company as a vehicle for new opportunities.

Call it market muscle memory, but the Parkit situation reminds me of what happened at Sitestar (now called Enterprise Diversified). Sitestar was a floundering microcap taken over by a group of value investors (Steve Kiel, Jeff Moore, and others). After cleaning house, they began converting the company into a publicly-traded alternative investment vehicle.

The company seeded Alluvial Capital, the hedge fund started by Dave Waters (OTC Adventures), along with several other funds. The company also invested in a HVAC rollup vehicle and acquired Jeff Moore’s portfolio of single family homes in Lexington, KY.

The excitement over this pushed the stock well above its tangible book value. But as you can see on this CoBF thread, things went sour.

Jeff Moore’s real estate empire proved to be less attractive than when purchased, and he was forced out as Chairman. The fund seeding has gone well, but the HVAC rollup results are less than stellar.

It would be interesting to see Leonite convert this company into a new Sitestar. However, this dream of building a new Berkshire or Leucadia remains elusive at the microcap level (ex. Ballantyne Strong, Biglari Holdings, Paragon Technologies).

Additional Rights Offerings From Insiders

Leonite and the other company insiders recently participated in a rights offering/private placement. With the stock selling for 50 cents on the dollar, this was a great opportunity (for them) to build up their position.

The structure of the rights offering is also interesting. Due to Canadian securities law, only Canadian-resident shareholders were entitled to participate. US-domiciled Leonite participated via a separate private placement, but Parkit’s other major shareholders (all Canadian) were able to participate.

Additional rights offerings could be in the cards down the road. Especially if the liquidation proceeds stretches into the early 2020s. Outside investors may bail, pushing this illiquid stock down to 30 or 40 percent of tangible book.

Interest Rate Reset

If the long-awaited interest rate increase does occur, this could have an impact on the valuation of Parkit’s assets.

On the other hand, parking lots can be considered “rate reset proxies”. This is a term Delaney uses in the Proactive Investors interview to describe one of the pros of parking lot investing.

“Rate reset proxies” is his term for assets that can quickly reset prices in an inflationary scenario (another example would be self-storage). This would allow them increase cash flow and maintain their valuation even if cap rates rise.

Bottom Line

Parkit presents an interesting opportunity for microcap investors to indirectly participate in a REPE (real estate private equity) investment. With Parkit’s investment in PAVe generating a 15% preferred IRR, the longer it takes to sell the portfolio, the more potential upside for Parkit shareholders.

On the other hand, there is good reason why Parkit trades at a heavy discount. Parkit holds a portfolio of parking properties that could be difficult to unload.

A haircut from the investor presentation valuations may be needed to move the Colorado and Connecticut properties. “What next?” is another good question before considering Parkit. Do the major investors in Parkit intend to fully liquidate, or are they interested in turning the company into a public vehicle? Will we see Sitestar-style diversification that doesn’t go as planned?

Parkit is not a high-conviction idea, but it is a buy for my portfolio. I’ve included it in my basket of nanocap deep value plays. With so few obvious value opportunities in today’s market, Parkit may be a strong consideration for your deep value portfolio as well.