Revisiting Keweenaw Land Association (KEWL): The Annual Report and the Once Every 3-Year Appraisal of its Timberland Are Out

Accounts I manage hold shares of Keweenaw Land Association (KEWL). I’ve written about it twice before:

Keweenaw Land Association: Buy Timberland at Appraisal Value – Get a Proxy Battle for Free

And

Why I’ve Passed on Keweenaw Land Association – So Far

I didn’t continue to pass on Keweenaw Land Association. Like I said, the stock is now in accounts I manage.

There are really two things worth updating you on. One is the annual report. The other is the appraisal. The appraisal is something the old management team – the one that lost last year’s proxy vote to Cornwall Capital – always did as well.

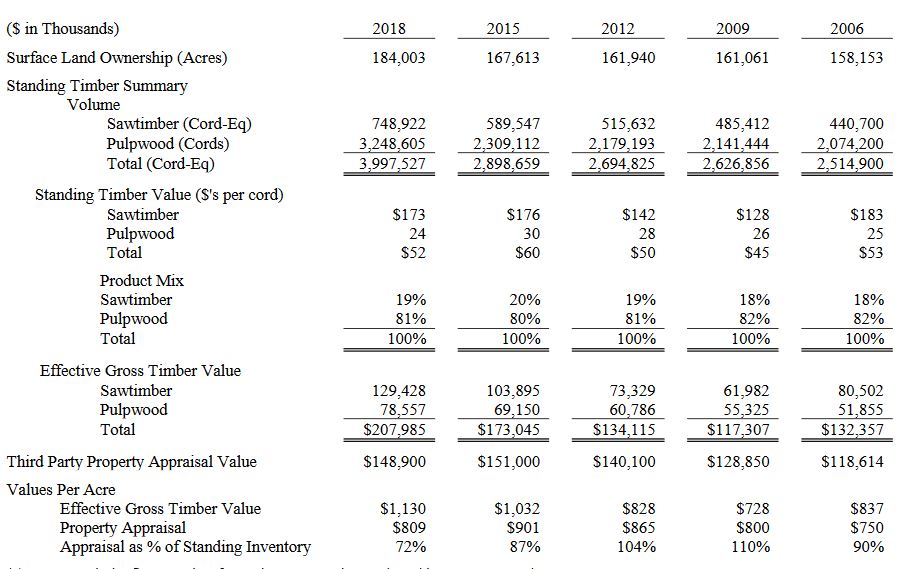

So, I can show you a summary of every appraisal from 2006 through 2018. The company includes this in its annual report:

You can read the entire annual report here.

You can read the entire annual report here.

A full summary of this year’s appraisal and methods used by the appraiser can be found here.

In today’s article: I’ll focus on the appraisal, because valuation of the stock seems to be the thing readers are most interested in. The annual report is also quite interesting though. The company’s new management is disclosing far more than the previous management. Although Keweenaw stock is “dark” (it doesn’t file with the SEC) – this latest annual report reads like a typical 10-K filed with the SEC. The company also changed its auditor to a better known firm (Grant Thornton) that audits plenty of other public companies.

As you can see in the table above, the value per acre of KEWL’s timberland was appraised at $809 this year versus $901 in 2015. That’s a decline of 10% versus 3 years ago. It’s also basically flat with an appraisal done in 2009 (so nearly 10 years ago). These are also nominal numbers. So, that means that the real value of KEWL has declined on a per acre basis over the last decade.

What’s tricky about this though is the last row you see “appraisal as a percent of standing inventory”. As you can see, the effective gross timber value – this is the value of all of the wood on Keweenaw’s land less the estimated gross costs of cutting and trucking that timber away – has risen pretty consistently. It went from $728 an acre in 2009 to $1,130 an acre today. But, the appraisal as a percent of that standing inventory went from 110% in 2009 – meaning the appraiser was then valuing the timberland above the gross value of the timber itself – down to just 72% this year. You can also see that the physical volume of timber – measured in cord equivalents – has compounded at something like 4% a year over the last 12 years. So, physically there is more timber on Keweenaw’s land every 3 years – and at least in the 2012, 2015, and 2018 appraisals this timber’s value has also increased per acre every time. However, the property’s appraisal has not. In fact, it declined by 10% these last 3 years. That’s clearly due to the change in the appraisal relative to the standing inventory.

Why has that happened?

Well, there’s some discussion of it in the appraisal summary. The appraiser notes that they would normally put greater weight on the “comparable sales approach” rather than the “income capitalization approach” (basically, a 10-year DCF). However, in this case they weighted the two appraisal methods equally.

As I’ve mentioned in past articles on KEWL – I prefer the comparable sales method. I don’t like the income capitalization approach. And you can read the details of the assumptions made to do that DCF for the income capitalization approach in that appraiser’s summary report. It relies on some solid assumptions like the growth – in fractions of a cord – per acre each year. But, then it relies on assumptions I don’t like such as the use of a 5.5% real discount rate. This may be a reason why the comparable sales approach gives a higher appraisal than the DCF based approach. In today’s environment of 2% inflation, a 5.5% real discount rate is equivalent to a 7.5% nominal discount rate. The problem with that can be seen by applying such a discount rate to the S&P 500 – it wouldn’t hold up well at its current price (in other words: I don’t expect the stock market to return 7-8% a year in the decade ahead – and I certainly do expect it to be more volatile than timberland). For comparison, inflation protected 30-Year U.S. Treasury bonds yield 1% right now. So, for appraisal purposes – the timberland here is being discounted at a 4.5 percentage point spread over U.S. Treasuries. This is what happens when you use DCFs. There are other even more speculative assumptions built into this appraiser’s DCF such as a 10-year holding period by any financial buyer, the decision by such a buyer to more aggressively harvest the timber at first, etc.

Since I could do my own DCF just as well as an appraiser could – I prefer to look at the comparable sales approach. An appraiser is much better able to judge the location of KEWL’s land, the quality of its trees, road access, etc. than I possibly could. An appraiser also knows the potential buyers much better than I do. So, this is the number I care about.

But, before I talk about the comparable sales approach – let’s do the math on the actual appraisal put out in this report. The appraisal is for $148.9 million. KEWL has 1.3 million shares outstanding. So, that gives a per-share appraisal of the timberland of about $114. KEWL has about $10 a share in net debt – I’m deducting both cash and securities (these are stocks KEWL holds) from gross debt. So, we have an appraisal net of debt of about $104 a share. In the annual report, KEWL’s management gave a “fair value” disclosure of several assets. The only other one that matters here is the mineral rights. This is a lottery ticket. If a mine is built soon and the price of the copper extracted is high – KEWL would earn good royalties. I have no idea if this will happen. KEWL’s management estimates the mineral right are worth a little over $5 million – or about $5 a share. So, you could look at this appraisal as saying KEWL stock is worth either $104 a share or $109 a share. It last traded at $79.50 a share.

Like I said, I prefer the comparable sales approach. The difference between the comparable sales approach and the income capitalization approach is large – it’s about $22 million (which is $17 a share).

The sales comparison approach alone – not blended 50/50 with the income capitalization approach as the appraiser did here – would give an appraisal of $160 million (instead of $148.9 million). If you divide $160 million by 1.3 million shares you get $123 a share. You then subtract the $10 a share in net debt. You’re left with $113 a share. If you want to add the $5 per share in mineral rights – you get $118 a share.

How would I do it?

I’d use the comparable sales approach alone. And I would assign no value to the mineral rights. This gives an appraisal of $113 a share. I’d then apply the standard “Ben Graham margin of safety” approach of buying only at 2/3rds of what you think something is worth. In this case, that’s $113 * 0.67 = $75.71.

This leads to the following buy, sell, and hold suggestions.

When KEWL’s stock price is…

Under $75: BUY the stock

Between $75 and $113: HOLD the stock

Above $113: SELL the stock

The stock last traded at $79.50 a share. So, it’s a hold. But, it’s something to watch.

It’s also worth mentioning that the appraiser lays out 6 cases in that report. The lowest end of the most conservative method is the low-end estimate using the income capitalization approach. It would give a valuation of about $80 a share. So, about today’s stock price. The highest-end estimate using the comparable sales approach would instead say there is about 95% upside in the stock. So, it varies a lot.

Even though the lowest end of the least favorable appraisal method still gives you a valuation per share of about $80 a share – without including mineral rights – which is right in line with today’s stock price, KEWL is not risk free. The company does have a lot of debt relative to its actual cash generating ability. This is supposedly considered safe for a timberland company. For example, MetLife is basically extending credit to KEWL based on the safety provided by the amount borrowed not exceeding about one-third of the value of the timberland. By that measure, the company is not over indebted. Right now, the timberland might be valued at like 10 times the net debt. But, timberland generates very little cash flow each year. So, this is definitely not a company with as strong a balance sheet, liquidity position, etc. as something like NACCO (NC). There is some financial risk here. So, even if there appears to be no “price risk” in the sense that the appraiser didn’t consider any scenario where the timberland would be worth less per share than where this stock currently trades – this stock is not risk free.

I wanted to focus on the appraisal here. The annual report was actually very encouraging. The only two questions with this new board are:

- Will they issue too many stock options to insiders

- Will they cut down too many trees too fast

Within reason: neither #1 nor #2 is necessarily a bad thing. By volume, they increased the harvest by more than 20% this year – and this board wasn’t even in charge all year. It was the biggest harvest in the company’s history. The company didn’t use equity grants as an incentive in the past. I have nothing against compensating management, the board, etc. in stock and based on performance. However, stock grants dilute the percentage ownership of investors like us. Basically, if you grant 1% of a company to insiders each year – you are lowering the total return in the stock by 1% per year forever.

There are a lot of encouraging signs out of this management. There is a lot more talk of value creation and eventual value realization. There is a ton more disclosure. And the plan to pay down debt is a good one. Apparently, they will be doing an investor presentation and Q&A for shareholders. This will also be made viewable by investors who don’t attend the annual meeting in person.

With this new board, KEWL has gone from a “dark” stock that didn’t reveal as much to investors as a typical SEC reporting company would to now being among the most communicative OTC stocks I’ve seen.

It’s a big change. But, a bigger investor relations push makes sense when the board is controlled by a hedge fund that owns a lot of shares.

Keweenaw mentioned that “now is not the time” for a sale of the company. They are open to offers. But, it’s not a good market for timberland transactions. The appraiser said the same thing. The appraisal report mentions a couple “no sales” including KEWL’s own attempt to sell all of itself (under the previous board). Apparently, there has been very little activity in terms of timberland transactions in the region within the last 2-3 years. This is a part of a bigger national trend. Many institutional owners of timberland have gone from being net buyers to being net sellers. I don’t know how much this has really affected prices at which transactions are done. But, it’s clearly dried up volume.

In fact, this recent trend – of extremely few major timberland transactions – is why the appraiser blended the income capitalization method and the comparable sales method 50/50 instead of relying primarily on the comparable sales method.

So, I wouldn’t say there’s any catalyst in KEWL.