It’s All About the Long Term: Amazon’s 1997 Shareholder Letter

“Jeff Bezos is the most remarkable business person of our age, I’ve never seen a guy succeed in two businesses almost simultaneously that are really quite divergent in terms of customers and all the operations.” – Warren Buffett

I really do agree with Warren in the statement above. Anyone who knows me, knows I am a complete Amazon advocate. Not only does my firm own Amazon stock, but I am a frequent user of the website and really have developed into some sort of fanboy. It is a company that, in my opinion, is virtually certain to be bigger 5-10 years from now than it is today. Every year it leaves me flabbergasted that Amazon continuously knocks it out of the park. Companies that are doing 100B+ in revenue annually should not be continuously growing sales by 25+% per year. To me it is extraordinary. And it is certainly a case study in action that we can all learn from and add to our investing-wisdom toolbox, whether you are a shareholder or not. But before we talk about the present, I think it can help all of us as investors to go back to the beginning and study the company. After all, investing is all about pattern recognition. The beauty of hindsight is that it’s always 20/20. Let’s use this hindsight to our advantage and learn from it.

In this series, we are going to go back and review every Annual Letter to Shareholders written by Jeff Bezos. I really encourage everyone to do this yourself here. I have printed off every Shareholder Letter and have read them multiple times and, like any good literature, I take away something new from it each time. When reading, I encourage everyone to continuously ask yourself this: “Is there any information in this writing that I can take with me to make myself a better investor?” One of the greatest things about investing is that we are constantly learning and all information in life is relative –meaning you can read books completely unrelated to business, read newspapers, watch movies, you name it, and still take away some sort of insight or wisdom that can relate to investing. That’s essentially what we are trying to do here at Focused Compounding; compounding both capital and wisdom. If you have not already, I deeply encourage everyone to read the book “The Everything Store” by Brad Stone. It is a great book that will help you get familiar with the beginnings of Amazon, and more specifically with Jeff Bezos as a CEO.

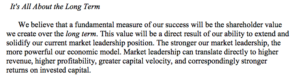

Let’s go back to 1997 when Jeff Bezos wrote his first letter to shareholders. Anyone who is familiar with the company will know this letter serves as the groundwork of principles that Amazon still embodies today. In fact, Jeff has posted the 1997 letter at the end of every Letter to Shareholders every year since writing it to keep the standards top of mind.

A manager who doesn’t just talk the talk but actually walks …

Read more