Jubilee Holdings Ltd: East Africa’s Largest and Most Profitable Insurer is Hidden Behind a Thinly Traded Stock

Jubilee Holdings Ltd: East Africa’s Largest and Most Profitable Insurance Company Is Hidden Behind a Thinly Traded Stock

By John M. Kamara

JUBI(Ticker Symbol – “JUBI” in Nairobi) is an insurance holding company listed on the Nairobi Stock Exchange since 1985 that owns and operates an 82 year old insurance operation across the East African region. As of June 28, 2019 the company has a market cap of US$290million (Ksh29 billion). In my view, the stock offers a decent investment opportunity for a buy-and-hold type investor because of the businesses quality combined with the discounted price the shares seem to trade at. I believe this price is available because of an “illiquidity discount”.

Incorporated in 1937, Jubilee Insurance was the first local Insurance Co set up as one of the initiatives by the then Imam of the Nizari Ismaili to revive the East African economies following the world recession of 1932. Sir Sultan Mohamed Shah Aga Khan III was the 48th heteridtary Imam of the Nizari Ismaili which is a branch of the Islam faith commonly referred to as the Nizari’s. The “Nizari’s’’ are a global, multi-ethnic community whose members are citizens from many parts of the globe.

This ‘group’ is involved in development, social and economic work through the Aga Khan Development Network (AKDN) that in turn carries out its activities through a multiplicity of its agencies. Its agencies are involved in sectors ranging from education to health, finance and even investment.

The AKDN is currently under the leadership of His Highness Aga Khan IV, the 49th Imam of the Ismaili Muslims who is the grandson of the Sultan.

The insurance company was one of the many business interests the AKDN would establish or invest in as part of their wider goal to improve the “quality of lives of the people/community” through its agency, the Aga Khan Fund for Economic Development (AKFED). This agency has been investing in for-profit businesses over the decades with potential to improve the lives of the members of the communities the businesses operate in. This type of investing has been more recently been termed Social Impact Investing (SII).

So in 1937, the Aga Khan called together a few prominent Ismailis from all over East Africa to join him start a local insurance company. The Company began with a small office in downtown Mombasa and today is now the largest composite insurer in East and Central Africa with annual premiums of $US 260million and $US670 million in float as of year 2018.

The listed company is an insurance holding company, Jubilee Holdings Limited (JUBI: NAI) which underwrites general, life and pension business through majority owned subsidiaries in Kenya, Uganda, Tanzania, Burundi and Mauritius. Its subsidiaries, whose businesses are split into General (what is more commonly referred to as Property & Casualty in many parts of the developed world) and Life Insurance companies, all rank in the top 3 or 4 in market share in their respective jurisdictions. In addition, JUBI began operations in the Democratic Republic of Congo (DRC) in 2015 through a partnership with state-owned insurance company, Sonas to offer medical and life cover products. However I don’t think the business results of this partnership have been material given the lack of mention in the any of the annual reports or earnings releases since 2015. In aggregate, the holding company underwrites more business than any other insurer in the region.

The Industry

The insurance industry in the region has about 60 players but less than 10% control over 60% of the market. Most of these players are small companies underwriting one or two risks (usually motor and fire). The biggest composite insurers in the region are Jubilee Insurance, Britam Holdings Ltd, ICEA Lion Limited, UAP Old Mutual Holdings Ltd and APA Insurance Limited. The Industry has had mixed results with underwriting losses in some years and underwriting profits in others. Insurance penetration is very low (1 – 4% of GDP) but the industry has been growing. In 2018, Kenya, the region’s biggest economy and Jubilee biggest market recorded annual premiums of $US2billion while Uganda, Jubilee second biggest market booked $US192 million in annual premiums.

Insurance products and services are not so popular in East Africa because the products are fairly complicated and the majority of the population is illiterate or semi-liberate. Like most developing nations, many don’t understand the need of insurance. However, the industry has been growing fast as the growth in the economies brings the increased need for insurance products and services.

The biggest insurers in the region have been in the industry for longtime, have massive sales forces, network of partnerships and the financial capacity to underwrite lines of business the smaller players can’t. As you probably know, insurance is a commodity business and therefore establishing competitive advantage is very difficult. However, if an insurance operation is run in a conservative way, understands insurance risk and can sacrifice short term growth for profitability then the shareholders of that business may own something worthwhile.

Past Performance, Economics, the Good and the Bad

To properly analyze the insurance operations of JUBI, you need break it up into three business units that are distinct albeit connected. The units are general insurance (P/C), life insurance and investments. When you look at the income statement of the holding company, it aggregates all the items from the three units of the consolidated subsidiaries. In fact, the regulations in most countries it operates in have already instructed insurers to have their general and life business done in separate limited companies. General insurance comprises of lines of insurance like fire, motor, marine, workmen’s compensation and the largest, medical insurance while life consists of individual/group life polices and pension administration. ‘Investments’ refers to the investment operations of the float generated by the two units described above.

As you probably know, the insurance business model is a float business which boils down to a ‘collect now – pay later’ model. Insurers turn this float into a revolving fund where by $1 paid out (settled claims) is simultaneously being replaced by another $1 of new business being written (collected premium) making it seem like the money never left. This money stays with the insurer who invests it for the benefit of the shareholders. However, to turn an operating profit, this business must pay out less than it receives annually (or over time).The difference between the two figures will be the cost of its float. A negative cost means it’s making an operating profit that can be added to the revolving fund (float) and increase income from investments which further grows the float and this creates a compounding effect. A positive cost on the other hand means the business is paying ‘interest’ to have this revolving fund. The ideal insurance operation makes money from both underwriting and investments while growing the size of its float.

JUBI premium revenue is currently spilt about 67% from general insurance and 33% from life & pensions business. The general insurance unit has made underwriting profits every year in the last decade while its life insurance unit has done the exact opposite – lost money every year since 2007. Worse yet, the underwriting loss from the life business has been greater than the profit from the general insurance business every year in the last decade. This means it has had an overall underwriting loss each year over the last decade. So, one part of its insurance operation is very good, another is terrible.

The life business includes guaranteed funds, life cover and pensions. I think the life insurance business is very difficult because the risk you cover per policy can be very long term. The pricing of these policies are based on very long term and very unpredictable variables like future interests rates. This is a key variable in the pricing of an insurance policy. The East African region‘s economies are typically developing ones and have been rocked with turbulent political and economic changes in the past decades, they have had revaluation of currencies, changing monetary policies, times of hyperinflation etc. This is not the kind of environment you want to sell a life policy in because the current price may look good today or even 5 years from now but then turns into a terrible one in the subsequent 10 years of the policy and you are on the hook for it. Combine that with players undercutting prices to gain share and you’ll end up with a horrible business.

A look at other life underwriters confirms the struggling economics of underwriting life insurance. Britam Holdings plc, the biggest life underwriter in the region had $US100 million (Ksh.10.76bn) in net premiums of life insurance in 2017 and made an underwriting loss of $US 30million (Khs.3.15bn). ICEA Lion Life Assurance booked net premium revenue of $US68 million (Ksh.6.8bn) and made an underwriting loss of $US74 million (Ksh.7.4bn). I find it interesting that no single listed insurance company in East Africa explicitly discloses their underwriting results in their annual reports or annual filings with the exchange. The numbers have to be worked out from the financials footnotes. A few of the letters from managements in the annual report mention the underwriting results but with a lot of ambiguity. I think the regulator should probably put some emphasis on such disclosures.

So why does Jubilee or and its competitors bother selling life insurance?

Underwriting life polices creates longer term float that can be invested in longer term investments that should potentially earn better returns. You may not be able to invest float from general business in say properties or private equity. Therefore life insurance companies are potentially able to earn better long term returns on their float than a typical general insurer underwriting say fire and marine insurance would earn.

A glance at the segment reporting of an insurer’s annual report shows that the bulk of their investment income comes from the life insurance float.

JUBI’s bottom line is green because the company is able to more than make up for the cost of its life insurance float via income earned from investing the float. I run that ‘’profit’’ figure considered only the actual cash received from its investment portfolio hence totally disregarding the fair value gains/losses on its portfolio in an attempt to be conservative. I figured it will suffice given they have reported fair value gains in 10 years out of the last 15 years.

The net result (combination of general, life insurance operations and cash returns from investment portfolio) is positive for 12 out of the last 15 years. This should give the investor an indication of the company’s earning power.

Moving over to the more pleasant part of the business, Jubilee’s General Insurance business has been making underwriting profits for the last 10 years demonstrating its ability in this line of business. A large portion of its general business (45% of net premiums in year 2018) is from medical insurance and this is what sets its underwriting operation from the pack. Jubilee’s medical business is the largest and the most profitable in the region.

Annual Insurance Industry Report (Kenya) for year 2017 showed Jubilee ranked number one in profits from medical insurance having made $US8.5 million (Khs851m) while the second best made about half that and the third best only 10% of that. The industry report for 2018 is yet to be released but an article in The Business Daily Africa on May 13, 2019 run a story about Kenyan insurance companies blaming doctors for the losses they incurred under medical insurance in 2018. The article mentioned that in 2018, Jubilee Insurance Kenya booked the biggest underwriting profit in medical of $US 7.7million (Khs771m) and followed by CIC Insurance with $US1.7million (Khs179m).

Medical insurance has been growing nicely over the last decade in East Africa. Industry reports for Kenya (East Africa’s biggest economy) show annual net premiums for the industry under medical line of insurance grew at an 18% annual compounded rate for the 5 years ending 2017.

The reasons for this growth are fairly obvious. The region has a rapidly growing population that has limited access to quality and affordable healthcare and the governments have failed to come up with a workable public healthcare plan that reaches out to the masses. Medical insurance provides a practical solution to this problem. The growth you see in medical insurance premiums has been an attempt to solve this problem. I believe medical insurance is a fundamental service in the society because most people cannot and won’t be able to afford the necessary healthcare and it attempts to solve that problem. That gives medical insurance as a service, durability. Unfortunately, underwriting medical insurance is not a simple business in the least. A company or group of companies could be selling a very durable and useful product that society depends on and yet they are hardly able to produce satisfactory returns on their shareholder’s capital. Think airlines. This is the case with medical underwriters in the region. They provide a crucial service to society and have experienced exponential growth in premiums but their shareholders can’t say the same about their profits.

The case for Uganda is not very different. Industry data shows medical insurance has been growing at a 20% annual compounded rate for the 5 years ending 2017 and just like the Kenyan market, medical underwriters in Uganda are having a hard time underwriting it profitably.

How has Jubilee been able to underwrite medical insurance so profitability for several years?

No publically available information gives an adequate answer to that question but my best guess, on top of generally sound underwriting principles, is that JUBI has been able to leverage off the ultimate controlling shareholders’ (Aga Khan Development Network) vast experience and expertise in the health care services industry. The Aga Khan group through its agency the Aga Khan Health Services, has been managing and running hospitals for over 90 years via a network of international hospitals based not only in East Africa but other areas of the globe like Asia. It also operates very many health centers, dispensaries and other community outlets. So the Aga Khan Foundation is very well vast with health care service provision and how the healthcare industry works.

This puts JUBI in a unique position to underwrite medical insurance that comes in form of decades of expertise, partnerships and in-depth knowledge about the healthcare industry through the AKDN. This must have a lot to do with why it’s been able grow its medical business and do so profitability. Last year, the management mentioned that the holding company intends to separate its medical business from general insurance to give it more focus.

Investment operations

As we’ve seen earlier investment income makes up the majority of the businesses earnings. As with most insurance companies, the investment operations are “liability driven’’ – meaning the primary purpose of the investment portfolio is to meet any payoffs required by policyholders from time to time. Therefore, the insurance regulatory authorities provide investment guidelines which give strategic asset allocations and limits through which insurance companies can invest their float.

Just like with underwriting performance, the listed insurance companies annual reports do not provide details of their investment philosophies or even report the returns on their portfolios in a standard way that is comparable. Again, the investor has to dig through the financials to get a picture of how their portfolios are doing. From what I can see, JUBI’s investment portfolio is run more prudently than most of its peers.

Last year several large insurers had some significant underperforming investments in their portfolios showing a less-than-conservative approach in their investment management.

For example, its close peer, UAP Old Mutual had to make impairments on corporate bonds they issued by the now insolvent ARM Cement Ltd and from the deposits they held in the collapsed Bank M of Tanzania. They also wrote down the value of some of its properties after aggressively investing in properties in the recent past signally either an earlier overstatement of their initial values/gains or their property investments have actually produced subpar returns.

Also, Britam Holdings plc blamed its 2018 pre-tax loss on investment write downs and impairments on some of its holdings. Sanlaam Insurance (formerly Pan Africa Insurance Holdings plc) also made write offs worth Ksh1.14bn in debt and equity notes they held in Kaluworks, Real People, Nakumatt (Distressed retailer currently in bankruptcy proceedings) and ARM Cement.

JUBI has not been victim of such events mostly because they seem to manage their float with prudence. The market has had many corporate bond issues that didn’t work out but never has Jubilee been invested in any of these issues that went belly up. They did not rush into commercial property like most insurers did in the last 5 years probably because they had already made strategic investments in commercial property decades ago in the central business districts of Nairobi and Kampala. Currently there is an oversupply of office space in Nairobi city and the expected returns on commercial property are not looking that great.

However, what really stands out is their private equity portfolio where they buy equity stakes in private companies alongside their anchor shareholder Aga Khan Fund for Economic Development (AKFED) and therefore these companies are reported as associate companies of the holding Co, JUBI. These private investments are usually in profitable, cash generative business ventures that pay JUBI dividends annually. For example, it has a 27% stake in Bujagali Energy Limited (BEL) that financed and built the 250MW Bujagali hydro power plant in Uganda. This has earned JUBI an Internal Rate of Return (IRR) of 15% over the first 10 years through cash distributions. Another successful investment is their stake in IPS Cable Systems Ltd, the holding Co for the famous meat processing brand, Farmers Choice. As a shareholder, it has collected cash dividends from since 2009 imputing an impressive IRR of 21.4% over that holding period.

JUBI is able to do these private equity deals primarily because it’s part of the Aga Kahn Group. The Aga Kahn Group has been a major investor in East African regional economies for decades. The typical East African insurer would not be able to participate in such well-structured private investments.

Just like with their medical insurance business, their investment operation has an edge over their competitors from the anchor shareholder.

As you may have figured, the AKFED is very instrumental in the management of JUBI. Their expertise in healthcare gives the Company the ability to maneuver the difficult field of medical insurance. Their wide portfolio of private investment deals across the region gives Jubilee an opportunity to deploy its capital in profitable ventures that are not accessible to many other investors. At the helm of the Company is Mr. Juma Nizar who served as the Board chairman for the last 17years. He is an AKFED executive who also chairs the Industrial Services Promotional (IPS) Group, an investment vehicle for the AKFED. This makes me believe he plays a major role in strategic management of Jubilee investment operations.

On the side of insurance operations, a regional CEO was hired in January 2018, (Dr. Julius Kipng’etich) to lead the regional operations of Jubilee Insurance in the five countries it operates in. Aside from that, each subsidiary typically manages its own insurance operations with a board and senior management in place.

I believe it’s the executives from Aga Khan Fund for Economic Development (AKFED) that keep the holding company intact, drive key decisions like investment and capital allocation decisions. The annual reports contain a only a letter from the Board Chairman and not the regional CEO and he is also very active during investor briefings and earning release presentations explaining a lot about the business and its strategy.

Capital Allocation

The company has maintained a simple and consistent policy on capital allocation. ‘’Simple and consistent” is a trait I look for in public companies and I believe outside shareholders should consider this a plus. The company returns back money to shareholders via cash dividends and once in a while, a bonus issue of shares. The cash dividend has been relatively low and this I believe has been in spirit of keeping the company well capitalized through internally generated funds so they do not have to borrow or raise more money through stock offers. The company has grown organically without raising additional capital or borrowing since 1985. In my view, this is a positive on the repute of the management and shows that the business is being run for the long term owner. As an outsider, you can be fairly comfortable as to how the company will allocate capital in the future – retain majority of the earnings (to strengthen capital base that can fund growth without having to borrow or restructure the balance sheet), pay a consistent dividend and issue additional bonus shares once every five years or so.

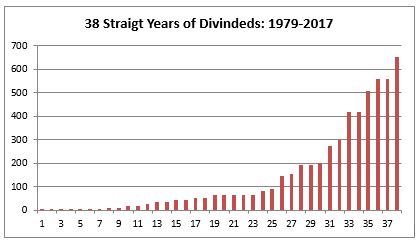

Jubilee holdings has paid a consistently increasing (no dividend paid in any single year has been lower than the one paid in the previous year) dividend every year from 1979 to 2018. The dividend has grown at an annual compounded growth rate of 15.8% during that 38 year stretch. That is not a dividend record you come across every day.

Valuation

This is the tricky part. There is plenty of misjudgment in putting a ‘’value’’ on business because we have to make assumptions about a future we aren’t certain about. By definition, the ‘’value’’ of any business will be the cash the owners will receive from it between now and judgment day. Despite it being the clearest definition of value we have, its implementation for the investor is very problematic. If you buy a business today and tomorrow its intrinsic value starts shrinking through poor capital allocation or changing economics, the valuation you made yesterday is a now a dinosaur. Before investors fire up Ms Excel to do a DCF, they should first check the odds that the business they are about to value won’t start eroding value in the near future. If you think the odds are medium to high that this could happen – I wouldn’t bother with the valuation.

The common statistical metrics and models that analysts love to use produce a false sense of correctness and brilliance and this doesn’t make our problem any easier to solve. None the less, l will attempt.

As a long term buyer, I tackle valuation from the standpoint of what price I’d buy out the minority shareholders and become a business partner with the majority or principal shareholder. Assume if you will that AKFED invited you to buy the 63% it didn’t own of the company but with the contingency that it will retain effective control by make all the operating, strategic and capital allocation decisions, would you be comfortable paying the current market price?

The answer to that question is based on a few key variables and numbers. These would include;

- The company writes about $US 260 million or so in annual gross premiums

- Shareholder’s Funds/Book Value is currently $US 280 million

- Annual cash dividends will be at least $US 6.5 million

- The company has float of $US 670 million that will probably continue to grow at about 10-15% per year.

- The company can earn at least $US 30 – 40 million off its float each year based off the current level of float assuming zero growth in float.

- The company does not use debt to fund its operations, there have been no capital raises and dilutions from ‘new strategic partners’ and there is low probability this will happen.

- The company has a niche in medical insurance that’s the fastest growing line of insurance in the region.

The price for this entire business is $US 290 million.

That’s a P/B of close to 1, premium-to-market value ratio of close to 1.1 and a PE of about 7.

In the opening paragraph, I mentioned liquidity was the reason I thought the market was pricing this business unfairly. To put this in perspective, the company has 72.4 million shares outstanding and average traded volume over the last 12 months was 480,000 shares. That’s an annual market cap turnover of 0.7%. This is much lower than the average stock listed on the Nairobi Stock Exchange. This is a thinly traded stock. Among the reasons for this is the relatively high stock price the share trades at. The stock has the fourth highest price per share on the Nairobi Stock Exchange and this eliminates a lot of retail trading in the stock. I believe this illiquidity pushes the stock to a valuation that otherwise wouldn’t exist given the quality of its business versus its competitors.

By comparison, other listed insurers all trade at PE’s above 10 and P/B over 1.5 (for those that made losses I have taken the last year of profits) despite having lower quality operations than Jubilee. The only reason I can pin point for JUBI’s relatively low market valuation is the illiquidity of its stock.