Kingstone: A simple New York homeowners insurer

Kingstone Insurance

Kingstone Insurance (KINS) is a multi-line provider of personal and commercial insurance. The company distributes predominately through independent brokers and agencies with a high touch model. The vast majority of premiums underwritten today have been in the state of NY in home property insurance. More recently, the company has begun branching out into neighboring states such as Pennsylvania, Rhode Island and New Jersey.

What is unique about Kingstone is their willingness to operate with smaller rural agencies. While most insurance companies require significant minimum premium volumes for an insurance agent to qualify for commissions, Kingstone’s minimum for agents is 50k. This gives Kingstone a sticky and loyal base of independent insurance agents who originate new business for them year after year.

Kingstone transitioned from a mutual into its current form in 2009 and has since been growing premiums at 25% a year while producing a return on equity of 15-16% in years without hurricanes. When hurricane Sandy hit the New York area in 2012, they experienced mild losses but were still able to maintain a return of equity of 4%.

This streak continued up until the first quarter of 2019, when Kingstone had to restate reserves in its commercial lines business, where it was writing property insurance for small businesses. While commercial lines formed a minor part of their business, Kingstone clearly mispriced the risks here and had to restate its reserves, taking substantial losses. Fortunately, Kingstone has acknowledged its past mistakes, reorganized its claims management department and pulled back on new commercial business. The market however has reacted as if Kingstone’s business model is fundamentally broken. Over the next several quarters Kingstone should show that their core home property insurance business is just as profitable as it used to be and that it can continue its history of profitable growth by growing into adjacent states.

Underwriting

Kingstone has for a long time maintained a mix of roughly 80% personal and 20% commercial policies. As they have experienced reserving issues in the commercial segment, Kingstone will stop growing commercial policies and instead focus on its core homeowner and dwelling coverage business. Approximately half of their policies are written in Long Island / Westchester, with another 43% written in NYC. Long Island / Westchester is a particularly interesting market for Kingstone as major insurers pulled out of the market in the wake of Superstorm Sandy.

Thanks to an Ambest upgrade to A- in 2017, Kingstone is well prepared to continue its growth as this allows Kingstone to access a greater number of insurance agents to sell its home insurance product through (many insurance agents limit their insurance writing with companies that are rated A- or better). Kingstone has been growing premium at 25% per annum for the last several years and is likely to continue to grow premium by at least 20% per annum through a combination of growth in New York and Long Island / Westchester as well as expanding its agent base in upstate New York, Connecticut, Maine and New Jersey.

Kingstone’s producers value their relationship with the company because it can provide excellent, consistent personal service coupled with competitive rates and commission levels. Kingstone has consistently been rated by insurance producers as above average in the areas of underwriting, claims handling and service. In the last two performance surveys conducted by the Professional Insurance Agents of New York and New Jersey of its membership, the company was even rated the top performing insurance company in New York. In addition, while most insurers require at least $1 million in premium for agencies to qualify for contingent commissions, Kingstone’s minimum is $50,000. This way small rural agents can write lots of volume for them and receive full commissions without having to go through a wholesaler. Kingstone in turn is able to maintain a loyal agent base of independent brokers.

While dealing with small insurance agents directly is relatively more costly than dealing only with larger scale agents/wholesalers, the company is focused on keeping expenses to the minimum level required to properly underwrite its business and to effectively process claims. While the majority of its business is downstate, Kingstone’s offices are in Kingston, NY, a location which provides them with a significantly lower cost base. Kingstone has also developed online application raters and inquiry systems for its personal lines and commercial automobile products. This has brought them increased business submissions from producers due to greater ease of placing business with the company as well as streamlining parts of the underwriting process.

Reinsurance

Kingstone only reinsures 10% of its personal lines premiums via quota share. Ever since receiving it’s A- Ambest rating the company has been attempting to reduce its reinsurance cover as the policies it writes are highly profitable. In addition, Kingstone has bought excess-of-loss catastrophe insurance up to $450 million (a 1-in-250 storm event), retaining only the first $4.5 million of losses. Kingstone has been gradually reducing the amount of reinsurance it uses as the policies the company writes are inherently very profitable. However, should Kingstone’s Ambest A- rating ever be threatened, I would expect them to increase the amount of reinsurance purchased again to maintain their rating.

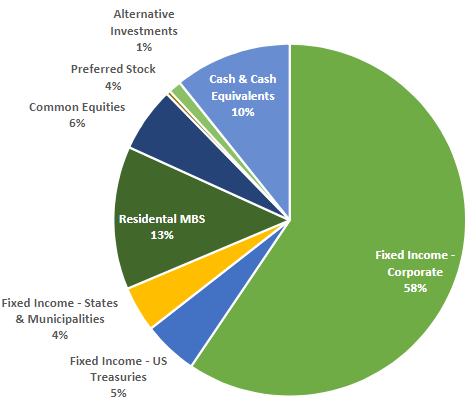

Assets

Kingstone takes a simple approach to investing its float. 90% of the portfolio is in fixed income instruments with an average duration of less than 5 years and an average rating of A-. The remaining 10% is split between preferred shares and equity investments. Raymond James manages Kingstone’s investments for them. With securities yielding 3.9% and an investments/equity ratio of 2/1 Kingstone can expect to derive about 5.5-6% of after-tax ROE from its investment portfolio over time.

Management

Kingstone’s chairman, Barry Goldstein, has been running Kingstone since 2001. Barry also owns 6.4% of the company. In 2017 Barry brought Dale Thatcher, the former CFO of Selective Insurance Group on as COO. In early 2018 Barry moved on to the role of Chairman, bringing Dale into the CEO role and effectively giving him control over day-to-day business decisions. While Barry is 66, he has not retired from the business. Rather, he will be focusing on broadening the companies’ distribution network and has been named CEO of KOCI, Kingstone’s new general agency. It’s too early to make a guess on fee contribution from this new venture but more details should emerge in the course of 2019. Bringing Dale on and paying him $1.3 million all-in, or about 2x his own salary shows Barry’s commitment to growing the company into a preferred Northeast multi-line carrier over the long term. I don’t think the incentive structure is great here with Dale receiving $500k in base, $300k from a 3% profit participation and $750K in RSA’s in 2020 but neither is it bad enough to be a dealbreaker. Barry had to pay up a little to bring a experienced CFO from one of the larger Northeast insurance carriers out of retirement onboard. We should see over the next two years whether this wager pays off or not.

Why does the opportunity exist?

Kingstone was on a good streak executing on its strategy of 20%+ premium growth, mid-to low 80s combined ratios and high teens RoEs until the fourth quarter of 2018. During that period a particularly cold winter led to numerous large pipe freeze claims on the home insurance side while Kingstone discovered that they had been under-reserving and underpricing their commercial risk in the first quarter of 2019. Management feels that they are adequately reserved after significantly strengthening reserves in the first quarter of 2019 and reducing the amount of commercial insurance written going forward.

Conclusion

Kingstone has guided to a 2019 combined ratio between 88-91%. In the longer term I would expect this to return to 86% or better. Meanwhile Kingstone can earn about 5.5-6% on their investment portfolio. In other words, Kingstone is an insurance company with sustainable after-tax ROEs of 15-16% and a reasonable growth runway. If Kingstone can earn a sustainable after-tax ROE of 15-16% a Price/Book ratio of 1.6x should be easily justifiable. If they can execute on continuing to profitably grow net premiums earned at 20% per annum, Kingstone is probably worth more than 1.6x book.

Risks

Frozen Pipe Claims: This is not the first year that frozen pipe claims have had a meaningful negative impact on results. The frequency of extreme weather events such as very cold winters is likely to be higher going forward than in the past due to climate change. While this is a risk, Kingstone can proactively work to educate its insureds on ways to prevent frozen pipes by adding insulation

Overexpansion: Dale has clearly been brought on to keep up the pace of expansion. In order to profitably expand, Kingstone needs to find underserved agents in rural areas in neighboring states, repeating the playbook it has successfully executed in New York. There is meaningful execution risk here, but bad execution should surface in the results relatively quickly as home insurance is relatively short-tailed