Norbit: A Norwegian Growth Company Trading At 8 Times 2019 EBITDA

by VETLE FORSLAND

In the middle of June this year, Norbit ASA (ticker: NORBIT) went public on the Oslo stock exchange at 20 kroner per share, after earlier aiming for an IPO price between 23 kroner per share and 30 kroner per share. It had in the first quarter introduced European truck drivers to a new digital tachograph, a device fitted to vehicles to automatically record speed and distance and landed a seven-year contract with the German industrial giant Continental Automotive – which controls 80 percent of the European market for tachographs. This contract helped Norbit’s ITS-segment (more on this later) make 36 million kroner in sales in the first quarter, compared to 40 million kroner for all last year combined. The company’s other segment, which produces sonar products, grew revenues from 28 million in Q1 2018 to 59 million in Q1 2019. Further, the company could boast about EBITDA-margins of 32 percent, bringing EBITDA to 50.1 million in the first quarter. Despite this, the initial interest in the stock seemed non-existent, bringing it to start trading at 9.75 times (conservative) 2019 earnings. Since then, two news articles have brought the stock price up 13 percent to 23 kroner per share – but this still adds up to a 2020 P/E of 11.5, a 2019 EV/EBITDA of 7.8, in an industry where the median peer trades at an EV/EBIT of 17.6 (Pareto Securities). The company is still illiquid, cheap and somewhat overlooked, with a market capitalization of 1,300 billion kroner, or ~144 million dollars.

Business overview

Norbit is a niche-technology company with operations internationally. They produce and provide tailored technology in several markets through three business segments. The company is located in the Norwegian city of Trondheim, known as a technology-heavy town, and has 250 employees (150-170 are engineers). Further, they have sales offices all over the world, and research departments in Budapest and Trondheim. The CEO, Per Jørgen Weisethaunet, was the third employee to work at the company, when he got hired as an engineer sometime in the mid-1990s. After working at Siemens for a couple of years, he became the CEO in 2001, and is currently the second largest shareholder with a stake of 11 percent of shares outstanding, after selling 4 percent of his stake in the IPO. The largest owner is the founder with 15 percent of the shares. As far as I can tell, it’s a very focused and able management. In a longer phone chat with CEO Weisethaunet, he told me that “We have ambitions of building a solid, large technology company with a focus on customized niche products”. “There are commercial genes in us that makes us want to constantly make money. Profitable growth is our focus”, he added. Norbit is aiming for a CAGR growth of 25 percent over the next three years, and Weisethaunet said that the first quarter paves the way for just that – at a minimum. Additionally, the company has been profitable for most of its years since inception.

Oceans

Their Oceans segment, that produces sonar technology, made up 35 percent of revenues in the first quarter of 2019. It’s the growth machine of the company and has doubled revenues every year since it was launched in 2013, including the first quarter of 2019. Sonar technology uses sound propagation for communication, subsea imaging and to detect objects at or below the surface, and exists in two forms: passive and active. Active sonars emit sound pulses and listens for echoes, and are considered the best way for detecting and locating subsea objects, while passive sonars listens for sounds from other vessels – often used in military settings. If you google something like “subsea sonar technology 3D”, you’d get a good look of what this is. The image these sonars produce are geophysical maps, so every point in the pictures are georeferenced. That means the viewer can locate the images to an exact location on the globe through geographical coordinates. Sonar technology is essential for dredging companies (removal of material underwater), environmental surveillance, contracting companies, researchers and scientists, certain offshore exploration and military operations. All the mentioned operations are often limited by deep water, debris, and lack of visibility, creating a demand for sonars.

The global sonar market is estimated to reach 3.7 billion dollars by 2023 (versus 2.6 billion today), but the company is focusing on certain niche markets that Norbit estimates to be worth 700 million: “There’s a lot of stuff happening in the industry that we don’t even touch. We have found niches where we can make a difference – we look for markets with scalability, but not too great – if the scalability is truly atmospheric, then someone other than us will take that market”, Weisethaunet told me. He added that they try to make technology that is difficult to make, and therefore difficult to hijack. Examples of niche solutions where sonars are needed are bottom mapping for an overview of what a sea, river or bay looks like on the bottom, for instance by being able to see if dredging operations are necessary in a place with boat traffic to make the traffic better; inspections of wells to see if there is an erosion; look for objects underwater; mapping of port areas underwater for construction or renovation for the harbor -the list goes on.

Everything needed in these sonar solutions can fit in a briefcase. This isn’t unique for Norbit – a similar company I have researched, Coda Octopus, make small sonars too, but in different markets (Coda is worth a look too, with terrific margins, growth, and a forward P/E of 11.5 and an EV/EBITDA of 14, though it traded at above 25 times EBITDA earlier this year). Norbit’s sonar solutions cost from 1 million kroner to 2 million kroner, which is cheap if you’re a large company that needs this product for an operation. Norbit tries to find small sales teams globally that get most of their revenues from Norbit, making the seller highly focused on these products, and equips them with high knowledge of sonars. Further, the Ocean segment has a diversified customer base, with the single largest client accounting for only three percent of sales. Additionally, oil and gas accounts for ten percent of sales, so the risk of an oil market collapse wouldn’t be that bad for Norbit. “In the Oceans segment we have had a very nice growth rate, but we are still a modest player in the market”, the CEO told me. “After all, we have only scratched parts of the surface”.

ITS

The Intelligent Traffic Systems segment, or ITS, makes up 23 percent of Norbit’s revenues. It’s a simpler segment than Oceans, and operates in a very different market from Oceans, but both require good technology in niche markets – however, the similarities mostly stop there. While Oceans is very diversified, with many small customers, ITS have few, large industrial giants with very large contracts. Luckily for Norbit, the company landed two important contracts in the first quarter of 2019 that are between five and seven years long. The two most important contracts are with Toll Collect and Continental Automotive.

ITS produces and distributes technology used in traffic. In Norway, they provide standard toll tags called AutoPASS, that let drivers pass through road toll areas without stopping. Most drivers in Norway have AutoPASS in their cars, and Norbit controls about 70 percent of this market. AutoPASS is mandatory for medium to heavy vehicles (above 3.5 tons) and Norbit has delivered 2.5 million tags like these since 2007. However, they barely get any revenues from this compared to their two flagship European products – digital tachographs and Short-range satellite communication for truck tolling.

The first one is with Continental, where Norbit produces tachographs for European truck drivers. Continental controls about 80 percent of this market. Basically, Norbit’s solutions allows government officials to read truck data for driving and resting hours wirelessly and digitally without stopping the car. So, a police officer driving by a truck or someone standing by the road, looking at a truck drive by, could read of the tachograph. On June 15th this year, a new EU legislation ruled that all trucks must have digital tachographs installed, in a move to transition to distance-based truck tolling (satellite). This opened a new niche market for Norbit, where the company can produce these short-range communication modules for distance-based truck tolling, that are integrated with the digital “smart tachographs”. As far as I understand it, these integrated solutions are provided to another large German company, Toll Collect.

For 2018, this segment had revenues of 40 million kroner, down 7.9 percent from 43 million in 2017. However, in the first quarter of 2019, this segment had its “step-up”, with the earlier mentioned contracts. In the first quarter revenues reached 36 million kroner, almost the entire sales number from the entire year prior, and EBITDA of 17 million kroner – margins of 47 percent. We will most likely see this quarterly growth continue throughout the year, before the segment will stabilize some. However, they could grow further in this segment as well, as they develop new products and find new niche markets within intelligent trafficking, as the EU continues to digitalize their traffic. This could come through broadening the customer base, or developing new DSRC (dedicated short-range communication) satellite solutions. After all, the global intelligent traffic market is estimated to be worth 23.4 billion dollars in 2018, and reach 30.7 billion in 2023 – that’s a CAGR of 5.7 percent. The growth is mostly driven by governments that shift focus to digital, more efficient traffic systems, increasing concerns for public safety and increasing traffic congestion problems. “The E.U. is now pushing for trucks to pay a fee per driven kilometer”, the CEO told me, which would widen their potential market, as DSRC solutions combined with smart tachographs would be a fitting alternative to today’s system. “Another advantage is that in a satellite based system, you have privacy with good security. No one wants to have data of where the truck is driving uploaded to a database that everyone can see. Instead, the data stays in the truck, and inspectors check only who has paid, and nothing more”, he said. All trucks in Europe registered after June 15th will have to install digital tachographs. The truck market is stable and growing, with close to 350 thousand trucks being registered in the EU on a yearly basis. In this market, Norbit has landed secure, long-term contracts that delivers about 18.5 million kroner in monthly revenues, with EBITDA margins at 30 percent and above (40 percent plus in Q1).

PIR

Norbit third and last segment is their wildcard. PIR – or Product Innovation and Realization – is exactly what it sounds like, a segment that does most of the research and development at Norbit. The company describes PIR as “an enabler for Oceans and IT, but it also offers R&D and contracting for long-term key clients”. So it serves as both an in-house research department, but also a segment that makes a profit through developed products that find its own markets, but don’t fit in either of the other segments. PIR has been making innovative products for nearly 25 years, and is based in three factories that date back to the earliest days of the company in the 1980s (before several mergers formed Norbit in the 1990s). Further, while PIR develops technology for ITS and Oceans and allocates resources to the two, it also offers R&D services and products to clients like Equinor, the largest oil company in Norway, Miros, Inda Nvia, Comrod and Kongsberg group, the largest industrial company in Norway. The department has created radar modules for sensor companies, antennas for Corvettes, DSRC (the technology used in the ITS segment) tags for local Norwegian vendors, developed the first sonars in 2013 and created systems that have been installed on the Snorre A oil platform for Equinor. About fifty percent of their manufacturing volume is directly related to Oceans or ITS, while the rest serves outside clients. So, it’s not a worthless segment, and the numbers can speak for themselves – PIR delivered revenues of 221 million kroner in 2018, down from 229 million in 2017, and generated EBITDA of 20 million in both years, giving a margin of 9 percent. Furthermore, the segment had revenues of 61 million in the first quarter of 2019 while EBITDA was 8 million. That’s a margin of 11,7 percent, with a top-line growth rate from the year before of 11,4 percent, while EBITDA grew over 14 percent. So, this segment has the highest sales of the three segments, but the lower margins makes it the lowest cash-flow generating business of the trio.

Quality and growth

I touched on both the quality of Norbit as a company and the prior growth rates of this company in the business overview – and what we see are two (and a half) different businesses sharing the same overhead but operating in different markets – with a supporting department in “PIR”. That means different types of clients, different margins and different growth rates. But, the company doesn’t really tell investors, in detail, how each segment looks on the inside. Still, it is possible to differentiate between the three, and find that their Oceans segment should be worth more than the ITS segment, while the ITS segment should be worth more than the PIR segment.

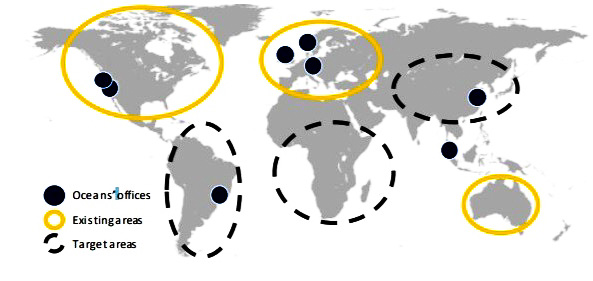

Firstly, there is the Oceans segment. The sonar market can be split into the submarkets of defence and commercial, where defence covers 60 percent of the market. Norbit focuses on the commercial market, which is expected to grow the fastest, with an expected CAGR of 8.5 percent, as sea trade traffic and maritime traffic increases with time. However, the company is “increasingly focusing on solutions aimed at the defence segment as well”, they say. Furthermore, the two sonar markets that Norbit are most active in – sonar for hydrography and sonars for underwater vessels (UUVs), – are expected to have a CAGR of 13.8 percent and 11.5 percent, respectively. Since its launch in 2013, Norbit’s Oceans segment has delivered a revenue CAGR of 105 percent, impressively mostly organically, except for two smaller acquisitions. “It has been a growth rocket-ship”, the CEO told me, but adds that it was easier to double the small revenue streams they had early on. However, the management is aiming for further growth through growing their product offering and grow its global distribution network – in the second quarter of 2019 they launched a sales office in China for the first time. We will see if the early stages of this launch has given results, when the company reports earnings for that quarter on August 22nd. Norbit lays down their growth strategy for Oceans in their prospectus:

“(i) Expand product offering by enabling clients to explore more in new market niches utilizing NORBIT’s sonar solutions.

(ii) Further strengthen NORBIT’s global indirect distribution network. This will be done by expanding the number of Tier 1 partners in its existing areas to strengthen its market presence and by targeting new selected regions. Figure 7.5.1 below displays the Company’s existing presence alongside its key target regions going forward.”

Additionally, now that Norbit has an established and proven, global sales network, the EBITDA CAGR of the last couple of years have been over 200 percent with margins of 20 percent plus, and most recently at slightly over 30 percent. The segment has a current market share of only 3 percent, and as long as the company can continue to find niche markets – which so far hasn’t been a problem – Oceans has the ability to grow double-digit for years, evidenced by the 110 percent year over year growth we saw in the first quarter 2019. The sonar segment is the future goldmine of this company, and has for the past years been the leaderships’ main focus.

Additionally, now that Norbit has an established and proven, global sales network, the EBITDA CAGR of the last couple of years have been over 200 percent with margins of 20 percent plus, and most recently at slightly over 30 percent. The segment has a current market share of only 3 percent, and as long as the company can continue to find niche markets – which so far hasn’t been a problem – Oceans has the ability to grow double-digit for years, evidenced by the 110 percent year over year growth we saw in the first quarter 2019. The sonar segment is the future goldmine of this company, and has for the past years been the leaderships’ main focus.

Moreover, the step-up that ITS saw in the first quarter with their valuable contracts, makes it another large source for profit for Norbit. Their long-term contracts for tachographs, with the market-dominating Continental and supplier Intellic will generate 200 million kroner in revenues yearly alone. So that’s 250 million kroner for 2019, with EBITDA-margins above 30 percent. After this year, Norbit is set for further growth through the recent EU regulation, as 350 thousand new trucks will be registered in the EU every year – these will need new, digital smart tachographs, and Continental controls 80 percent of this market. “You can see that this will result in nice volumes for Norbit”, the CEO said in a statement. On top of this, the company’s growth strategy as outlined in the prospectus marks two goals: finding new product opportunities in the ITS market and securing new long-term contracts:

(i) Develop and maintain NORBIT’s position as a supplier of DSRC solutions to satellite-based tolling OBU vendors. NORBIT is well-positioned in this segment due to its experience and ability to deliver tailored DSRC solutions.

(ii) NORBIT is to utilize its experience and competence to develop new applications of the short-range communications technology and to broaden the customer base. The development of DSRC modules for smart tachographs is a recent example of this.

«What we have said now, is that we aim to deliver a 3-year CAGR of above 25 percent, with and EBITDA margin of over 20 percent”, the CEO told me. Although EBITDA-margins was at 32 percent in Q1 (and profit margins of 21,5 percent), he says he wants them down towards 25 percent so the company can invest more in growth. For the first quarter, the Oceans segment had an EBITDA margin of 29 percent, ITS had 47 percent while PIR has 12 percent. “Our primary focus now is to deliver on inherently strong growth, and explore strategic opportunities primarily to look for companies that fit ITS and Oceans. We manage development and production well organically, but acquisitions are very relevant”, he said. Furthermore, the company will pay out between 30 and 50 percent of the company’s net income in dividends. If we use the free cash flow yield from the first quarter 2019, which was at 5.3 percent, we get a dividend yield of around 2.5 percent. Half of their annualized net income from the first quarter would equal a yield of 10 percent.

There are two things that are a drag on the overall quality of the company: Return on assets and historical financials. Norbit delivered outstanding numbers across the board in the first quarter, but ROA came in at “only” 8 percent, while the three-year average is 7 percent. I usually prefer companies that can provide reliable and high returns on capital, but 7 percent – where the return ranged from 2 percent to 12 percent – is neither reliable nor high. Over time, companies with a reliable return will compound faster than a less reliable return. Furthermore, the future projections and the very, very recent financials of Norbit are a lot better than what they have historically been. Sure, the company has made money in almost every year of its existence. But we have rarely seen the kinds of margins, yields and growth that Norbit has experienced in the past couple of years, and especially in Q1. That’s a major concern – it could mean an investment thesis is based on stories provided by the management, for instance. Or, it could mean that Norbit had some sort of a breakthrough recently, which is not unlikely. Norbit’s flagship business, the Oceans segment, was brand new in 2013, and tiny only a couple of years ago – it just became a meaningful part of the overall company last year. So, the company has spent years on building a new segment, spending 7-8 percent of their revenues on R&D (and still do), and expanding this new segment – before it finally paid off. In my opinion, Oceans have grown to become a business that can thrive by itself, with a lot of different customers globally, healthy organic growth, and great margins. Furthermore, Norbit landed their two major long-term contracts within ITS in the beginning of 2019 – two contracts that were game-changing for that segment. Does the lack of great historical financials make the stock riskier? Yes – but that doesn’t necessarily mean that what we know about Norbit’s recent past, and what we know are analytical, speculative guesses, are wrong.

Value

Therefore, I feel confident that we are dealing with a business that is above-average. Norbit has good growth rates, great profitability and durable products with an able management. Furthermore, insiders held 43,37 percent of Norbit stock as of July 29th, including a 10-percent stake by the founder’s family, and a 6-percent stake held by a board member. The founder owns 15 percent while the CEO owns 11 percent, even after selling shares in the IPO. So, they are putting money where their mouth is, which is another quality sign at this company. Norbit currently fluctuates between 22 and 23 kroner per share, and as of writing this, closed at 22.70 kroner per share Monday. What might be a fair value for this company?

There are many ways of finding that out. We can do a sum-of-the-parts analysis of the three segments, where Oceans deserves the highest multiple, followed by ITS and PIR. However, the fact that Norbit operates in niche markets within niche markets makes that somewhat difficult. Let’s look at the Oceans segment first, where we have several multiples to pick from: Broker Pareto Securities says peers adjusted for different growth rates trade for 15.8 times EV/EBIT. Further, a basket of eight mid-cap stocks that produce scientific and technical instruments trade at 25 times earnings. ITS doesn’t really have any direct peers, but our brokers tells us that peers trade at an EV/EBIT of 13 times, while PIR-peers trades at 7.5 times.

However, this is very speculative – instead we could compare the multiples of Norbit with that of an average business.

Norbit’s most recent EBITDA margin was 32 percent, but the CEO wants it down to 25 percent. So, let’s see how much EBITDA it could generate this year. Their new ITS contracts are expected to generate 55.5 million kroner each quarter this year alone – let’s say 50 million. If we add this to their 2018 revenues, we get 240 million. Meanwhile the Oceans segment generated 59 million in revenues in the first quarter of the year – assuming negative growth we get full-year revenues for Oceans of 220 million kroner. Let’s assume, to be conservative, that PIR generates 200 million kroner this year.

That equals to total 2019 revenues for Norbit of 660 million kroner, and with margins of 25 percent, an EBITDA of 165 million kroner, which means that Norbit trades at a 2019 EV/EBITDA of 7.9. This figure tells us that Norbit is – relatively speaking from the broad stock market’s perspective – undervalued. If we say that it deserves no less than the multiple of a normal business, then Norbit’s normal valuation is (165*10) 1.650 million kroner, as the company has no net debt. That equals to a fair share price value of (1.650/52,5) 31,42 kroner per share.

Let’s do the same on a P/E-basis. Norbit has profit margins of 21 percent, 16 percent if the CEO gets it his way and brings down margins. That is a profit of 105,6 million kroner. With a “normal” P/E of 15, we get a market value of 1.584 million kroner, or 30,17 kroner per share, an upside of 32 percent.

So, if Norbit closes this value gap within a five-year period, the multiple expansion will generate a return of 5.5 percent every year for five years. Adding a free cash flow yield of 5.3 percent and a conservative growth rate of 4 percent, we get an annual share price increase of 14.8 percent for five years. This is a lot more than one might expect from buying the S&P 500 index. Furthermore, these are conservative multiple numbers and growth numbers, to balance the possibility of an error in free cash flow yields (if the yield from Q1 was temporary). If Norbit comes through with a solid quarterly report on August 22nd, we will most likely see a re-valuation closer to 25 kroner and up. But, the most important thing here, is that Norbit has a clear margin of safety – it is an above average business trading at a 2019 P/E in the early teens.