PRAP Japan (2449): Japan’s Healthiest Public Relations Firm – Trading At Just 4 Times EBIT

This article originally appeared on Kenkyo Investing, a value-driven service specializing in Japanese small and microcap stocks. Each month, Geoff will pick his favorite article from Kenkyo Investing and share it with you here at Focused Compounding. To read all of Kenkyo Investing’s articles, visit Kenkyo Investing’s website and become a member. Don’t forget to use discount code “FCPODCAST” to get 10% off.

Write-up By Kenkyo Investing

Thinking Points

- PRAP Japan (TSE: 2449) is Japan’s fourth largest public relations consulting firm offering marketing communications, corporate branding, crisis communications, event management, and content production services to corporate customers in a variety of industries.

- Compared to its competitors, PRAP has the healthiest balance sheet and has delivered business performance at a consistently elevated level.

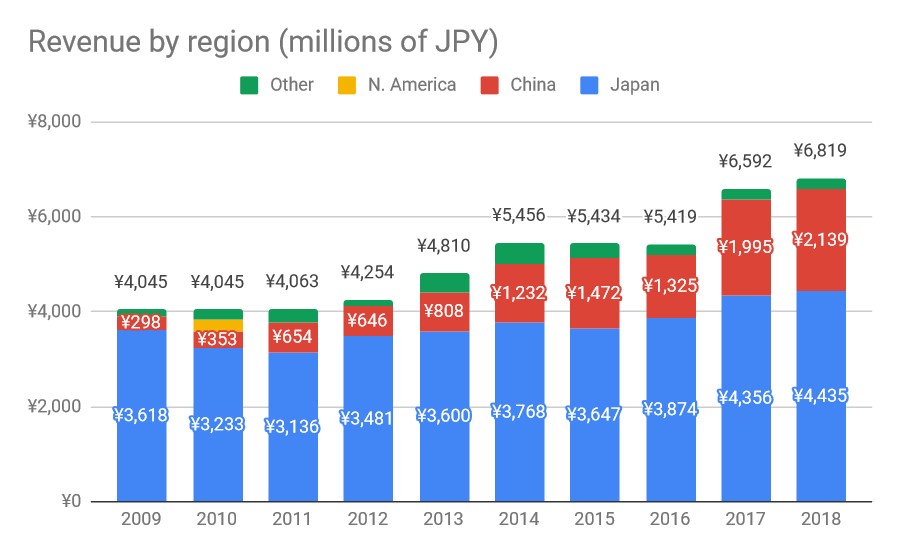

- Over the last decade, the company built its China business, which now accounts for nearly a third of consolidated 2018 revenues. Meanwhile, its Japan business has remained mostly stable, with modest growth. PRAP plans to expand in the Asia Pacific region going forward.

- Despite its consistently strong business performance and industry-leading balance sheet health, PRAP trades at an adjusted 4.3 EV/EBIT, considerably lower than its peers, which trade between 9.7x and 25x.

- Though there is no clear catalyst in sight, if investor sentiment shifts and PRAP trades at comparable multiples, investors can expect a three year investment CAGR of 21% with minimal business risk investing at today’s 1,599 yen per share price.

Introduction

PRAP Japan (TSE: 2449) is a public relations (PR) consulting firm offering marketing communications, corporate branding, crisis communications, event management, and content production services to corporate customers in a variety of industries. Founded in 1970, the company is among the older and established PR firms in Japan. Over the past decade, PRAP has increased its efforts in China, mainly targeting Japanese companies wanting to establish a presence in China.

Source: Company filings

Source: Company filings

Though PRAP offers a variety of services, it is a single segment company. As of 2018, PRAP is the 4th largest PR firm in the country by revenues.

The business & environment

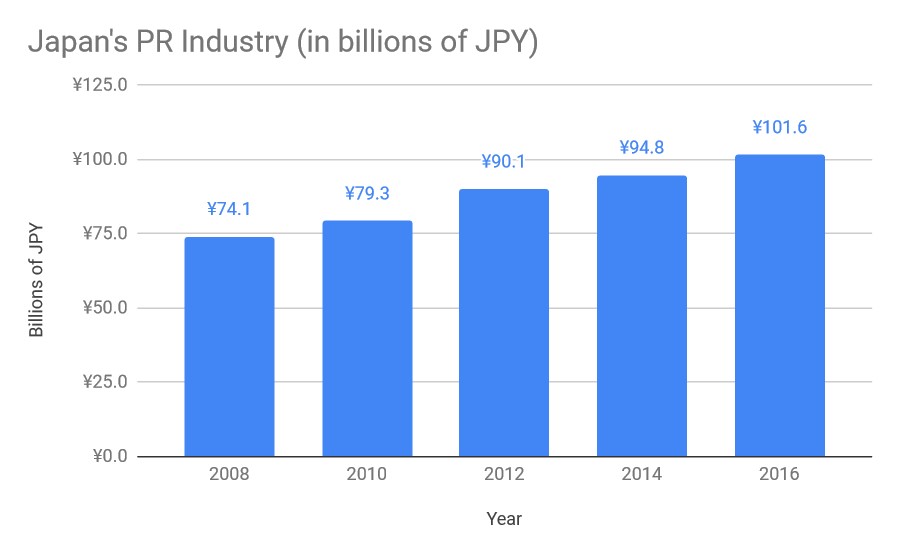

The Public Relations Society of Japan (PRSJ) estimates that the PR industry size in Japan was 101.6 billion yen ($90 million USD) in 2016 (Japanese). Long term historical data isn’t available for the industry as it is still small. That said, PRSJ notes that the industry is rapidly growing:

Source: Public Relations Society of Japan

Source: Public Relations Society of Japan

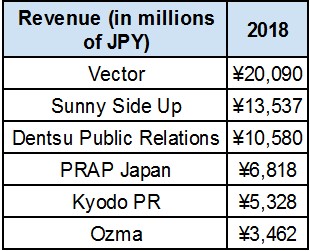

Over the last 8 years, the Japanese PR industry has grown at a 4% CAGR. In the last couple years, newswire services and video production and promotion services have fared particularly strong. The key players in the PR industry are:

Source: Company websites

Source: Company websites

Vector (TSE: 6058), Sunny Side Up (TSE: 2180), PRAP Japan, and Kyodo PR (TSE: 2436) are publicly traded. Dentsu Public Relations is under Dentsu (TSE: 4324), Japan’s largest advertising agency, and Ozma is affiliated with Hakuhodo (TSE: 2433), Japan’s second largest advertising agency.

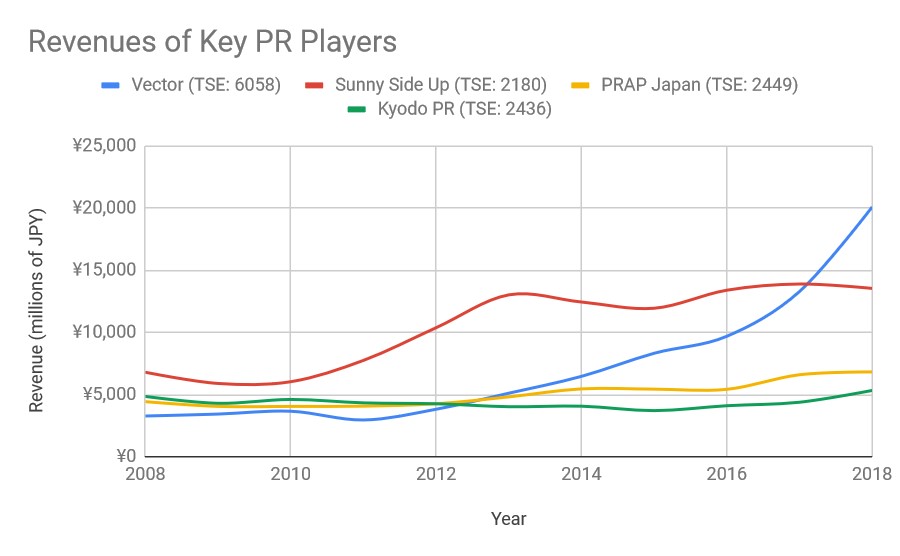

Although Japan’s PR industry has been growing quickly, PRAP’s revenue growth pales in comparison to Vector and Sunny Side Up.

Source: GuruFocus, chart created by author

Source: GuruFocus, chart created by author

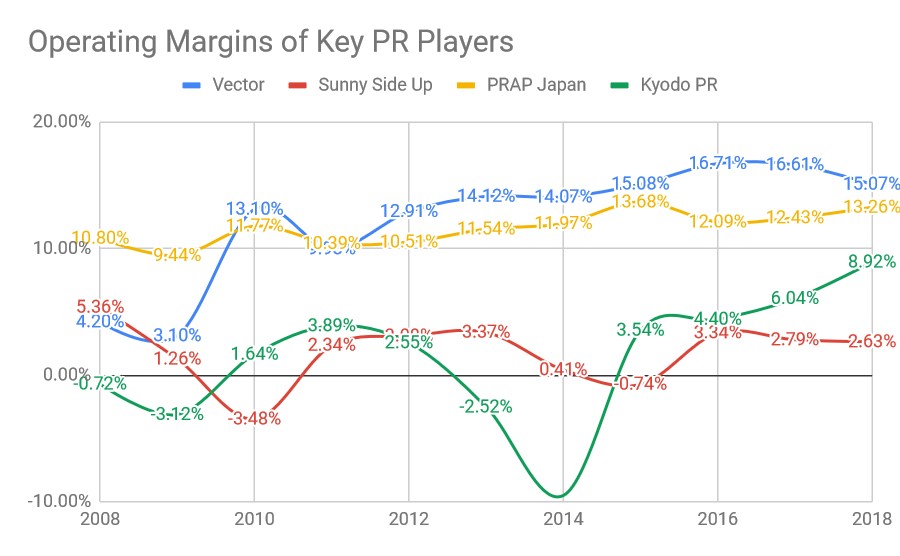

During the 2008 – 2016 period when the industry grew at an annualized 4% CAGR, PRAP’s revenue growth was at an annualized 2.6%. With that said, PRAP’s business has been the most stable, especially when looking at operating margins:

Source: GuruFocus, chart created by author

Source: GuruFocus, chart created by author

What’s particularly interesting about PRAP Japan is that its subsidiaries combined deliver stronger operating margins than its unconsolidated PRAP Japan business. In total, PRAP has 5 child companies and 1 grand child company.

Revenues from its China operations increasingly account for a bigger portion of combined child/grandchild companies. In 2018, China revenues (1 child company, 1 grandchild company) was 78% of combined child/grandchild companies’ revenues. One important note, however, is that the company only owns 60% of each company. The rest of the subsidiaries are 100% owned by PRAP Japan.

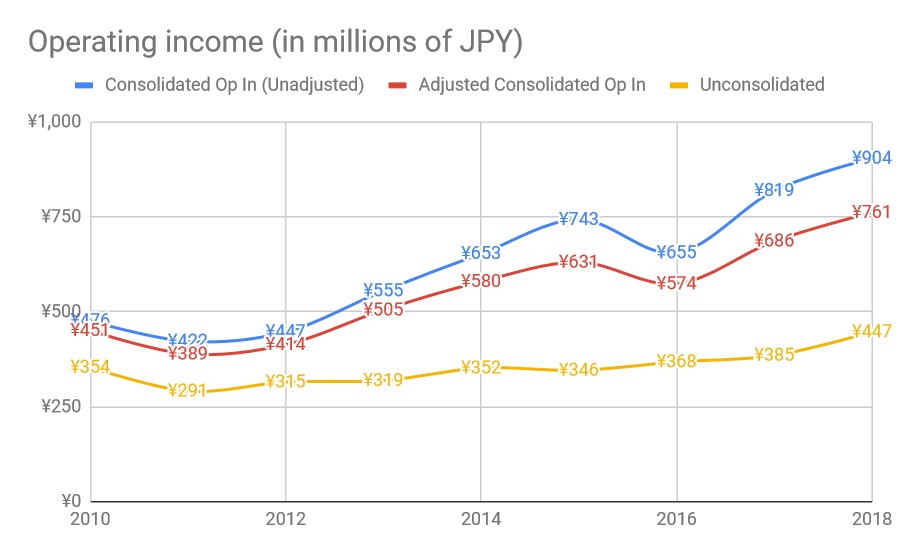

Since PRAP does not breakdown operating income by region, we can only estimate what adjusted consolidated operating income would look like. Assuming the percentage of China operating income to combined child/grandchild operating income is the same as the percentage of China revenues to combined child/grandchild revenues, adjusted consolidated operating income will look like this:

Source: GuruFocus, filings, author estimation

Source: GuruFocus, filings, author estimation

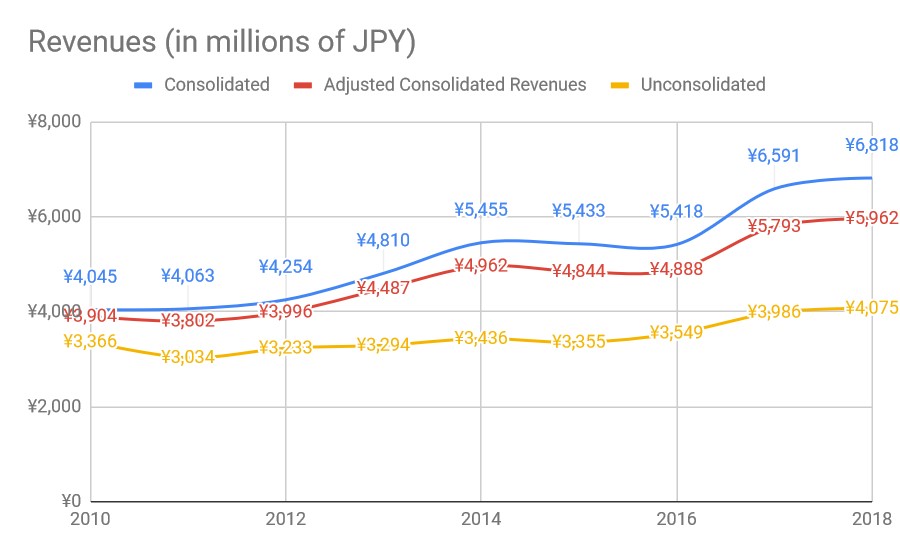

Here’s another chart to give you an idea of what adjusted revenues look like as well:

Source: GuruFocus, filings, author calculation

Source: GuruFocus, filings, author calculation

To be sure, the growth in China is nothing to sneeze at, even after adjusting for minority interest. Still, it is something to keep in mind when looking at PRAP as much of the growth, both in revenues and operating income, was driven by its China operations.

Where PRAP is headed

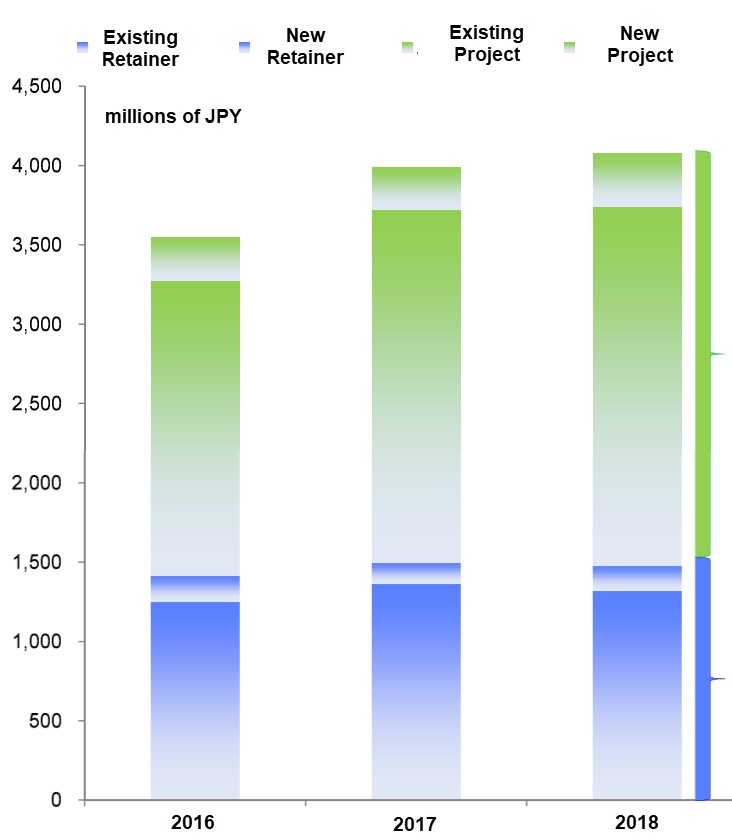

If there is one thing to note, it’s that PRAP is remarkably stable. Now, like many PR companies, PRAP also has two main forms of offering its services: on retainer or by project. Though the company does not disclose exact revenue figures for this, it does show a graph with the distribution (and no exact figures) in its presentation.

Source: 2018 presentation, translation by author

Source: 2018 presentation, translation by author

Keep in mind, these are unconsolidated revenues for PRAP Japan. Recent growth, as you can see, has mostly come from project based work, which is inherently shorter term than retainer contracts. While the increased project based work also means more opportunity to convert clients to retainer contracts, it appears this has not been the case between 2016 and 2018.

For fiscal 2019, management is guiding for 7,010 million yen ($62 million USD) in revenues (+2.8% YoY) and 920 million yen ($8.2 million USD) in operating income (+1.7% YoY).

Over the medium term, without any specific financial targets, the company plans to focus on industry specific PR, improving crisis and training offerings, and increasing support for foreign companies entering Japan for its core offering. For new business, the company is mainly looking at the Asia-Pacific region and digital platforms for expansion.

Shareholders

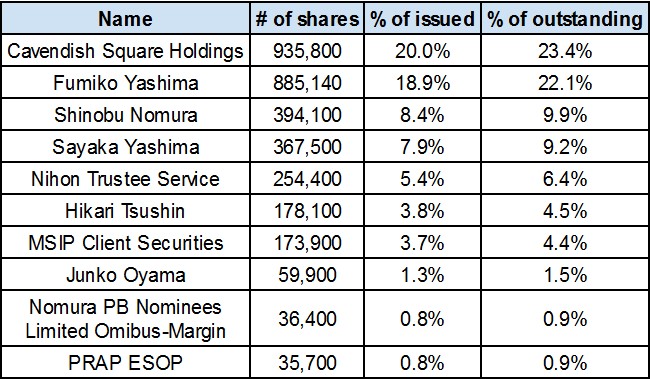

As of fiscal 2018 year end (August 31st, 2018), PRAP Japan had 4,679,010 shares issued and 682,827 shares in treasury, leaving outstanding shares at 3,996,183.

Here are the major shareholders:

Source: Company filings, Nikkei

Source: Company filings, Nikkei

Cavendish Square Holdings is a subsidiary of WPP (LON: WPP), a London-based multinational advertising and public relations company. The company has held shares in PRAP Japan since 2002.

The relationship between WPP/Cavendish is rocky. WPP/Cavendish proposed the removal of the CEO and one director (Japanese) in 2013 (shortly after the founder passed away), but this didn’t go through. Then in 2014, WPP sued the CEO & director (Japanese) regarding a financial advisory contract between PRAP and a securities company as well as attorney’s fees incurred during a corporate governance examination. WPP claimed a violation of duty of care and loyalty. The judgement went in favor of the CEO & director (2017, Japanese). Isao Suzuki assumed the CEO position in 2015. Neither the former CEO or the director are with PRAP Japan anymore.

Fumiko Yashima, Shinobu Nomura, and Sayaka Yashima are part of the founding family. Founder Hisashi Yashima passed away in late 2012, and the three inherited a significant portion of their current stakes.

Financials & Valuation

- PRAP Japan is one of the leading public relations companies in Japan, with arguably the most stable business performance as well as the healthiest balance sheet.

- While the company has seen healthy growth over the last decade, much of it has come from its China business, which isn’t wholly owned by PRAP. Moreover, its Japan growth skews toward project based work.

- On an adjusted basis, business performance is less attractive, though still respectable.

- Going forward, PRAP plans to focus on digging deeper into current offerings while expanding into the Asia Pacific region.

- Though without a clear catalyst, if PRAP trades at multiples similar to its competitors, investors can expect a three year investment CAGR of 21% with low business risk.

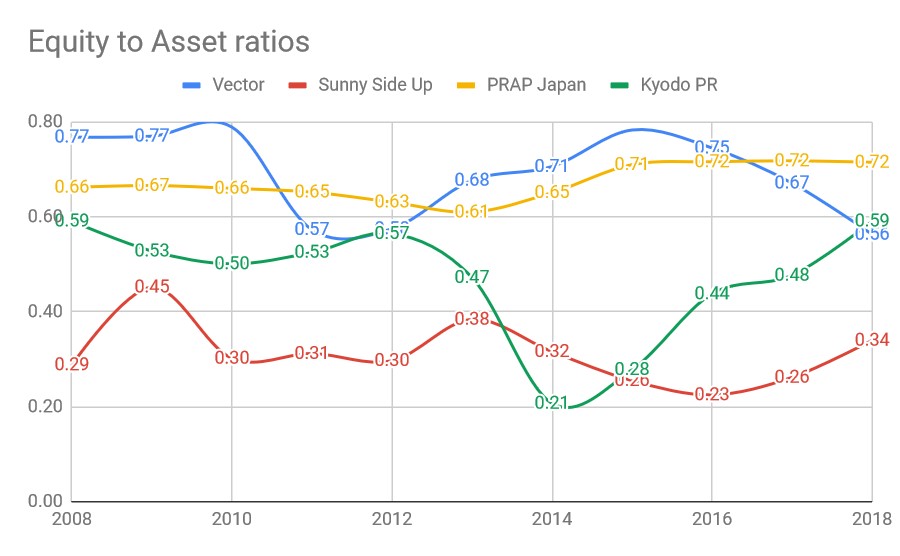

We’ve already established that PRAP is operationally among the healthiest PR companies in Japan. Moving over to the balance sheet, here’s what equity-to-asset ratio looks like for PRAP and publicly traded competitors:

Source: GuruFocus, chart created by author

Source: GuruFocus, chart created by author

Flashing Vector’s balance sheet against PRAP’s doesn’t make for an apples-to-apples comparison, mostly because PRAP is focused on PR and Vector, though still PR-centric, has its hands in 121 different startup ventures (7 of which have IPOd in the last 3 years).

64% of PRAP’s assets come in the form of cash. With no debt and negligible fixed assets, the company has a net cash balance amounting to 28% of market cap (at 1,599 yen per share). Current EV/EBIT, using operating income attributable to parent (adjusted for China), comes out to 4.3x.

Other than moving/improving the office in fiscal 2012 (~100 million yen, or $890K USD), PRAP hasn’t had any notable capital expenditures. The company has been comfortably free cash flow positive for over a decade, generally with a free cash flow margin above 5%.

To be sure, PRAP’s revenues and operating income did fall from 4,729 million yen ($42 million USD) to 4,045 million yen ($36 million USD), and 573 million yen ($5.1 million USD) to 382 million yen ($3.4 million USD) between fiscal 2007 and 2009. The company’s services aren’t immune to the swings of business cycles. Still, the company remained more than healthy throughout the global downturn.

Interestingly, EV/EBIT would still be 8.5x using 382 million yen as the EBIT figure. Vector trades at ~25x EV/EBIT, something you’d expect from a high growth, heavy venture investment business. Meanwhile, Sunny Side Up and Kyodo PR, with recently improving but still inferior to PRAP business performance, trade at 9.7x and 12.5x EV/EBIT, respectively.

If PRAP were to trade at 9.7x EV/EBIT, its share price would be around 2,600 yen compared to where it is today at 1,599 yen. Assuming no growth in the business over the next three years, cash accumulation of 200 million yen ($1.8 million USD) per year, and dividend payout of about 100 million yen ($890K USD) per year, investment CAGR should come in around 21% with low business risk.

Of course, a material investor sentiment shift like this tends to require a catalyst. PRAP is making a late entrance/focus into digital PR, however, the more promising business is likely its expansion into Asia Pacific, especially given its track record in China. The Singapore subsidiary, which the company recently formed, is 100% owned by PRAP. For now, there is no immediately clear catalyst, but the Asia Pacific expansion is worth paying attention to going forward.

The bottom line

PRAP, the 4th largest public relations company in Japan, is also the healthiest and most stable in the industry. Yet, its stock trades at EV/EBIT multiples considerably lower than its peers. Though there is no immediate catalyst for investor sentiment to drastically shift, if the company trades at multiples similar to its competitors, investors can expect a three year investment CAGR of 21% with low business risk.

This article originally appeared on Kenkyo Investing, a value-driven service specializing in Japanese small and microcap stocks. Each month, Geoff will pick his favorite article from Kenkyo Investing and share it with you here at Focused Compounding. To read all of Kenkyo Investing’s articles, visit Kenkyo Investing’s website and become a member. Don’t forget to use discount code “FCPODCAST” to get 10% off.