Goodness vs. Soundness

Tuesday, May 8th, Industrial Logistics Properties Trust (ILPT) by George Baxter

To Focused Compounding members:

Ben Graham wrote: “Confronted with a…challenge to distill the secret of sound investment into three words, we venture the motto, MARGIN OF SAFETY…all experienced investors recognize that the margin of safety concept is essential to the choice of sound bonds.”

Note the word I bolded: “sound”. As I sat down to write this memo, I thought immediately of chess. Can a good chess move be an unsound chess move? Can you win a game because you made a move that actually gives you a negative margin of safety? We know you can. After playing a game of online chess, humans often have a computer chess engine analyze their game. At each point along the way, the computer evaluates the position and states the advantage for black or white in terms of hundredths of a pawn. The computer can also suggest “lines” – or series of moves – where the game would have worked out differently. So, a computer can tell you what move your opponent should have made and whether or not you had a real advantage under “best play”. A move that wins against a human with limited time to think but would fail against a computer with infinite time to think may not be a bad move – but, it is a speculative move. The English word speculation comes from a Latin word – a language Graham knew well – that basically means “to look out for”. A speculation is future focused. It depends on stuff you have to look out for. In chess, to judge whether or not your speculative move was a good one you can look at the result of your game. However, to judge whether or not your speculative move was a sound one you have to sit down – perhaps with a computer, but certainly with a lot of time – and analyze what would have happened had a different move been played in response. Perhaps Graham’s most important quote on the topic of margin of safety is this one:

“The function of margin of safety is, in essence, that of rendering unnecessary an accurate estimate of the future.”

A sound move is one that works well enough whatever your opponent plays. A sound investment is one that works well enough whatever the future holds. But, just as some “unsound” chess moves work more often than not when playing against a human – some speculations have awfully good odds.

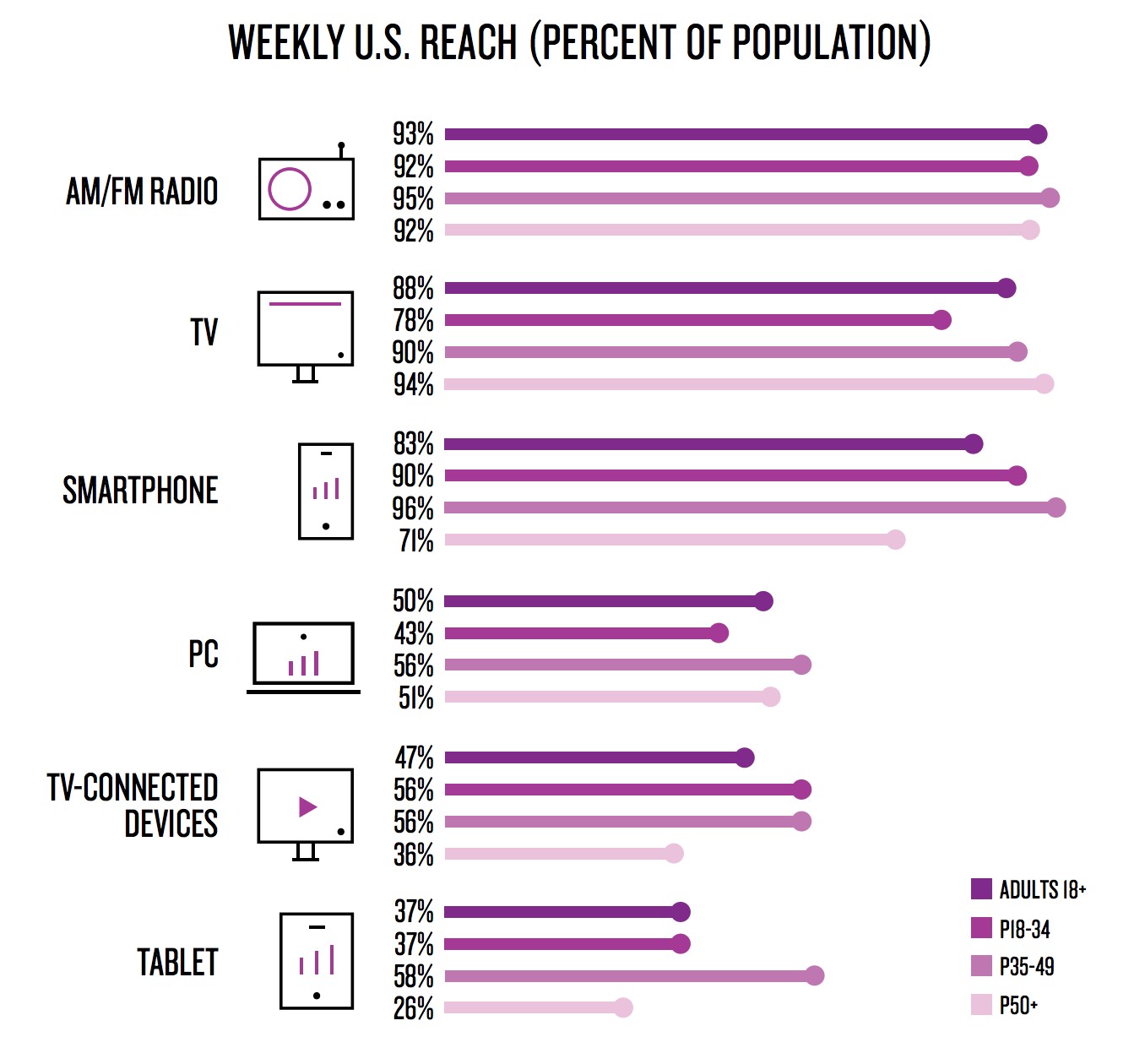

This brings us to Entercom (ETM). Last week, this minnow that swallowed the whale called CBS Radio was the subject of an excellent write-up by Vetle Forsland. A lot of members have asked for my comments on the stock. And a lot of members are clearly excited by the opportunity. Here’s the thing: If I had to come up with one and only one “line” that is most likely to be played out over the next few years, it …

Read more