He Who Has the Highest Opportunity Cost Wins (CAKE, NC, GRBK)

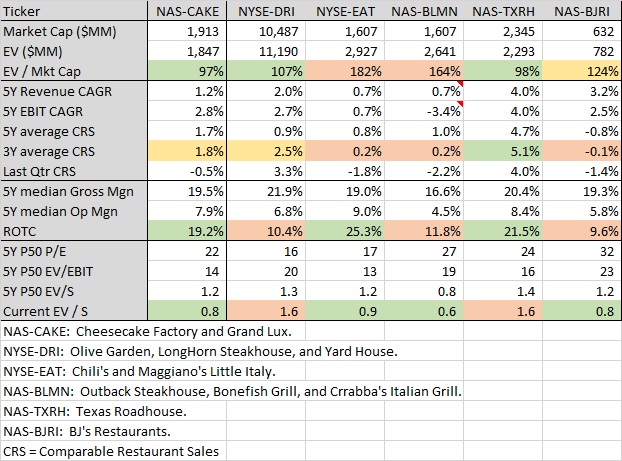

Someone who reads the blog emailed me about Cheesecake Factory (CAKE):

“Why are you not buying CAKE – it is around 66 cents on the dollar – at 40 dollars (a share)?”

When I answered that to his satisfaction, he asked:

“…So your options right now are most likely OMC, Howden and CAKE? You said in your OMC (stock report) that it was the best business you’ve ever analyzed. Is that still the case, especially compared to CAKE etc.?”

Omnicom is a better business than Cheesecake. However, Cheesecake may have more room to deploy capital within the business for the next 5, 10, 15 years. Apparently, Cheesecake management still thinks they can grow the concept from 200 locations to 300 locations. It’s not unheard of for them to open 8 new restaurants a year. So, that’s probably equivalent to 3% compound annual growth in the number of Cheesecake locations over a period of 10-15 years. Each location may be capable of earning a 10% to 15% after-tax return on the company’s cash investment of say $8 million to $12 million (they also sign a lease, but this does not tie up any shareholder money). Let’s call it $10 million per location in cash the company puts in and they can repeat that same $10 million bet at each of another 100 new locations – that’s $1 billion more in reinvestment done at rates of 10% plus.

To put this in perspective: Cheesecake may be able to re-invest 50% of its current market cap over the next 10 years at rates of return equal to or greater than 10% a year. It can also buy back its own stock. Both companies can do that and I expect both will do that aggressively. But, Cheesecake may have this additional opportunity to invest about 50% of its market cap over the next 10 years in the actual business at good rates of return. For Omnicom to reinvest 50% of its market cap on those same terms, there would need to be something in the $8 billion to $9 billion price range that will earn a year one 10% plus cash return on your investment.

I don’t see how Omnicom can find something like that. Right now, Omnicom can only compete with that kind of value creating capital allocation by buying back its own stock. Omnicom’s stock would have to stay cheap for a long time while the company gobbled up its own shares for OMC’s capital allocation to add as much value as Cheesecake’s capital allocation. So, Cheesecake may grow intrinsic value per share faster than Omnicom. Omnicom’s still the safer bet if you had to own one stock forever. But, if you have to own one stock for the next 10 years – I can’t promise that OMC has a way to deploy as much cash as profitably as Cheesecake might. Again, I stress might (CAKE needs to find good mall type locations to do this).

My options …

Read more