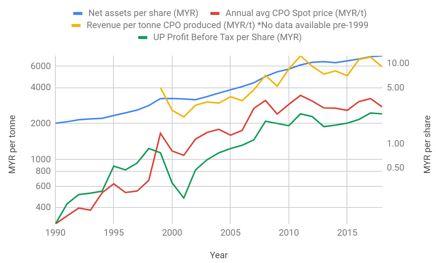

United Plantations: A Low-Cost Palm Oil Producer with 11 to 17% Returns on Equity and Excellent Capital Allocation

by WARWICK BAGNALL

United Plantations Berhad (KLSE:UTDPLT, UP for the sake of brevity) is an integrated palm oil plantation, milling and refining company (plus a small coconut plantation). It’s currently too expensive for me to buy but it is a company that I would like to own if the price ever drops to an acceptable level.

Superficially, there are a lot of reasons why palm oil companies look like a bad investment. Like all agricultural commodities, the price of palm oil fluctuates a lot. There’s the risk of pests, disease or unfavourable weather events. A significant amount of palm oil is used for biofuel so there is some regulatory risk associated with reduction of biofuel subsidies or an outright ban of biofuel. Many people have concerns about the health impact of consuming palm oil. And the industry has had a lot of bad press regarding forest clearing, peat fires and loss of wildlife habitat.

I have some pretty strong views on these areas. For full disclosure I previously worked in the vegetable oil industry (including palm oil milling) and still do a small amount of work for a palm fruit milling machinery company. So you could say that I’m biased but I have at least seen what goes on at well managed mills in Malaysia, Indonesia and PNG. My opinion is that most of the bad publicity is undeserved and that unless people everywhere decide to accept a major downgrade in their diet and standard of living, palm oil is going to be part of our diet for the foreseeable future.

Previously, most of the hard fats in our diet came from animal fats such as tallow, lard and milk fat. Vegetarianism (and also halal and kosher requirements) made the first of those two unacceptable for many consumer products and veganism reduced the addressable market for the third. For a period, hydrogenated seed oil (mostly soy) provided an acceptable alternative. Unfortunately, health concerns regarding trans fat meant that hydrogenated oils became unpopular. That left palm. For a large food manufacturer or restaurant chain seeking an oil which makes baked goods fatty (but not oily) or fried food crispy, the oil which will offend the least number of customers from a dietary and religious point of view is palm.

Palm oil (and palm kernel oil) are also very versatile (compared to the main industrial oils) in terms of producing specialty products. The oil can be fractionated simply by chilling it until part of the fat solidifies and filtering the solids out from the liquid. The wide range of fatty acids in the oil make it useful for oleochemicals such as soaps and emulsifiers. It’s currently a very cheap oil – that might not continue in the future. But it will probably always be the easiest oil to manufacture many specialty products from.

In terms of the environmental impact, palm has much less impact than other oils when managed correctly. Palm oil uses a fraction of the area …

Read more

This miniature is a Primaris Space Marine. Space Marines are GW’s single most iconic creations – armies of elite, genetically engineered superhumans wearing power armour and dedicated to defending humanity in a hostile galaxy filled with forces bent on humanity’s destruction. The full GW model range is simply vast though, which you can get an idea of by visiting the company’s web pages at

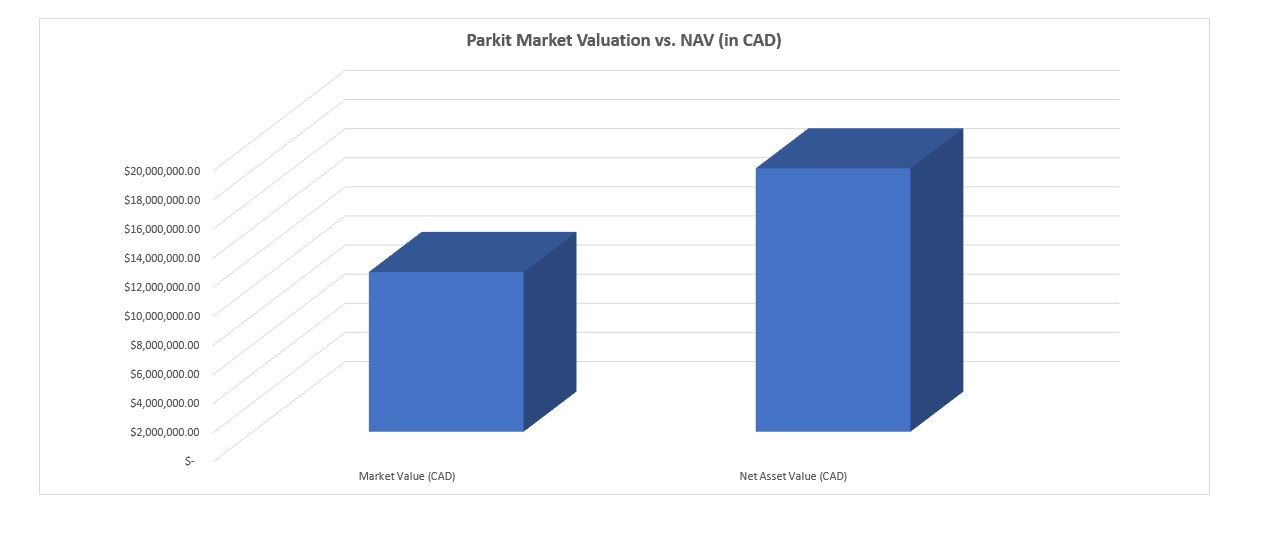

This miniature is a Primaris Space Marine. Space Marines are GW’s single most iconic creations – armies of elite, genetically engineered superhumans wearing power armour and dedicated to defending humanity in a hostile galaxy filled with forces bent on humanity’s destruction. The full GW model range is simply vast though, which you can get an idea of by visiting the company’s web pages at  (Image Created by the Author; Data via Parkit Investor Relations Page and Author’s Calculations)

(Image Created by the Author; Data via Parkit Investor Relations Page and Author’s Calculations) (Source: Parkit Investor Presentation, April …

(Source: Parkit Investor Presentation, April …