PRAP Japan (2449): Japan’s Healthiest Public Relations Firm – Trading At Just 4 Times EBIT

This article originally appeared on Kenkyo Investing, a value-driven service specializing in Japanese small and microcap stocks. Each month, Geoff will pick his favorite article from Kenkyo Investing and share it with you here at Focused Compounding. To read all of Kenkyo Investing’s articles, visit Kenkyo Investing’s website and become a member. Don’t forget to use discount code “FCPODCAST” to get 10% off.

Write-up By Kenkyo Investing

Thinking Points

- PRAP Japan (TSE: 2449) is Japan’s fourth largest public relations consulting firm offering marketing communications, corporate branding, crisis communications, event management, and content production services to corporate customers in a variety of industries.

- Compared to its competitors, PRAP has the healthiest balance sheet and has delivered business performance at a consistently elevated level.

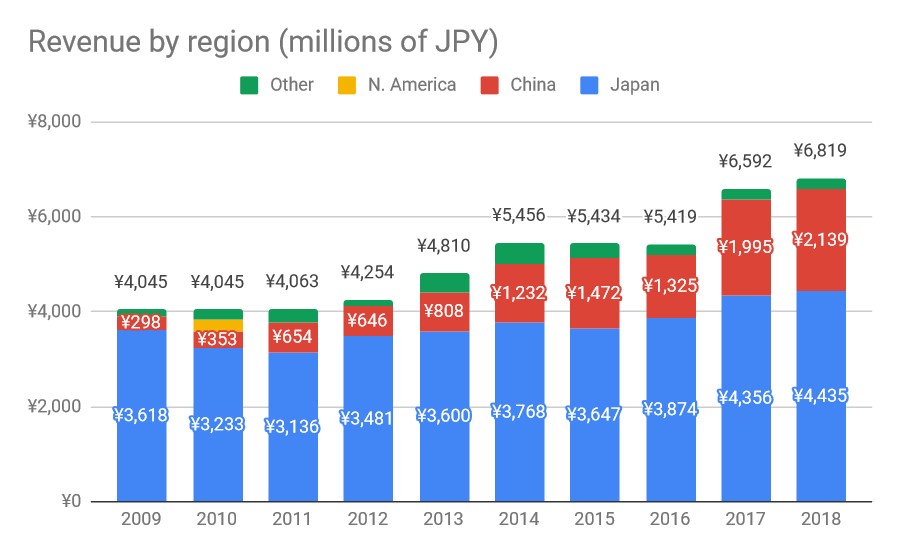

- Over the last decade, the company built its China business, which now accounts for nearly a third of consolidated 2018 revenues. Meanwhile, its Japan business has remained mostly stable, with modest growth. PRAP plans to expand in the Asia Pacific region going forward.

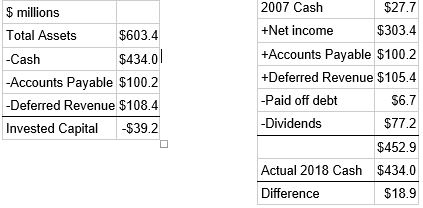

- Despite its consistently strong business performance and industry-leading balance sheet health, PRAP trades at an adjusted 4.3 EV/EBIT, considerably lower than its peers, which trade between 9.7x and 25x.

- Though there is no clear catalyst in sight, if investor sentiment shifts and PRAP trades at comparable multiples, investors can expect a three year investment CAGR of 21% with minimal business risk investing at today’s 1,599 yen per share price.

Introduction

PRAP Japan (TSE: 2449) is a public relations (PR) consulting firm offering marketing communications, corporate branding, crisis communications, event management, and content production services to corporate customers in a variety of industries. Founded in 1970, the company is among the older and established PR firms in Japan. Over the past decade, PRAP has increased its efforts in China, mainly targeting Japanese companies wanting to establish a presence in China.

Source: Company filings

Source: Company filings

Though PRAP offers a variety of services, it is a single segment company. As of 2018, PRAP is the 4th largest PR firm in the country by revenues.

The business & environment

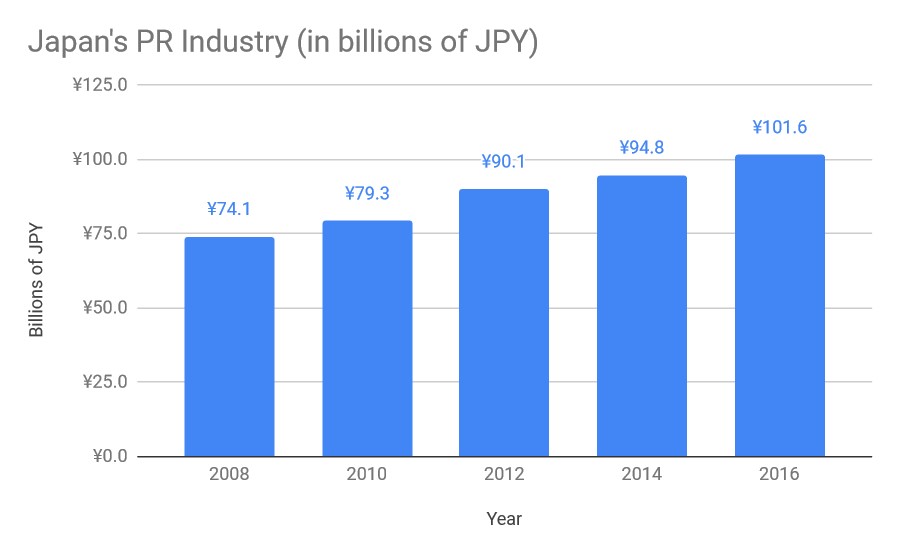

The Public Relations Society of Japan (PRSJ) estimates that the PR industry size in Japan was 101.6 billion yen ($90 million USD) in 2016 (Japanese). Long term historical data isn’t available for the industry as it is still small. That said, PRSJ notes that the industry is rapidly growing:

Source: Public Relations Society of Japan

Source: Public Relations Society of Japan

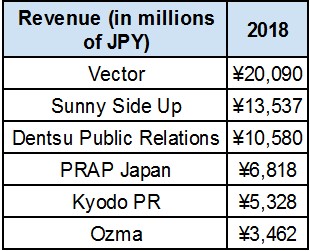

Over the last 8 years, the Japanese PR industry has grown at a 4% CAGR. In the last couple years, newswire services and video production and promotion services have fared particularly strong. The key players in the PR industry are:

Source: Company websites

Source: Company websites

Vector (TSE: 6058), Sunny Side Up (TSE: 2180), PRAP Japan, and Kyodo PR (TSE: 2436) are publicly traded. Dentsu Public Relations is under Dentsu (TSE: 4324), Japan’s largest advertising agency, and Ozma is affiliated with Hakuhodo (TSE: 2433), Japan’s second largest advertising agency.

Although Japan’s PR industry has been growing quickly, PRAP’s revenue growth pales …

Read more In addition to its home market, URC also has presence in 12 other countries in Southeast Asia and Oceania. Its major international markets include Vietnam, Thailand, Indonesia, Australia and New Zealand.

In addition to its home market, URC also has presence in 12 other countries in Southeast Asia and Oceania. Its major international markets include Vietnam, Thailand, Indonesia, Australia and New Zealand.